With so many calls for higher mortgage rates lately, now might be the perfect time to play contrarian.

It’s something I like to do in general, but it seems to work even better when the subject is “mortgage rates.”

Often when the consensus is high, things tend to unexpectedly shift and surprise everyone.

At the moment, everyone is in the higher-for-longer camp, so much so that it seems they can’t all be right.

And when it seems like there’s absolutely no hope in sight, the storm clouds part.

Lots of Headwinds for Mortgage Rates Right Now

At the moment, it seems like mortgage rates are riding a bicycle with a flat tire up a steep hill in the pouring rain.

Nothing seems to be going their way, whether it’s tariffs, the trade war, the big, beautiful bill (and all that government spending), the U.S. credit rating downgrade, and now even talks about Fannie and Freddie being released.

All of these things are contributing to higher bond yields, which directly impact long-term fixed mortgage rates.

The 10-year bond yield has risen markedly over the past three weeks, climbing from around 4.15% to 4.55% today.

It was as high as 4.60% yesterday, but has since cooled off. Still, that’s enough to put the 30-year fixed firmly back above 7% thanks to bloated spreads.

And every time the 30-year fixed climbs back above 7%, you can just feel the wind go out of the housing market’s sails.

The monthly payment difference isn’t huge, but the shift in sentiment in palpable.

However, what if I told you mortgage rates might still be on track to improve by later this year.

And that times like these are when we are most surprised?

Back to my contrarian point, it’s when a trade gets crowded that things tend to unravel. When everyone is so sure of something, in this case higher mortgage rates, they go the other way.

Zoom Out on Mortgage Rates for a Clearer Picture

I always like to zoom out a bit when speaking of mortgage rates. Too much can happen on a day-to-day basis, similar to the stock market.

Yes, mortgage rates can change daily, but it’s important to look at the longer trajectory for answers.

Just consider this chart from Mortgage News Daily for the past 24 months. There is a clear downward slope in mortgage rates, despite the recent volatility and upward movement.

There also tends to be an increase in mortgage rates every spring, which also happens to be the peak home buying season (go figure).

Meanwhile, mortgage rates tend to be lowest in winter when things are the slowest (also go figure).

That smartened me up for my 2025 mortgage rate predications post, where I made the adjustment for higher rates in the second quarter, before forecasting a move lower in Q3 and Q4.

My prediction is still in play and going according to plan, though it might be a bit delayed based on the many events that have taken place.

The Fed Is Staying the Course as the Drama Plays Out, Data Is What Matters

There have been a lot of surprises (and fireworks) thus far in 2025, but at the same time we were warned about all of this.

Everyone knew Trump winning the election would lead to tariff talk, trade wars, increased government spending, and so on.

Even the thought of Fannie and Freddie leaving conservatorship was in the playbook.

When it comes down to it, none of this comes as a major surprise. Everyone was told these things were going to happen, so you can’t be all that shocked.

This also explains why the Fed has been playing a slow hand, instead of panicking and cutting rates ahead of schedule.

However, they are still expected to cut, it’s just that the Fed rate cuts have been pushed out.

The same general outlook exists, a cooling economy with rising unemployment, which should lead to lower bond yields and rate cuts.

It’s just that because of all the drama and the months of trade wars, and the new tariffs, it’s unclear what the data will look like for a little while.

Chances are it’ll show increased inflation. But how much of it? And will it be enough to spark a return to 8% mortgage rates?

I watched a video from JPMorgan Asset Management fixed income portfolio manager Kelsey Berro and she did an excellent job putting everything in perspective.

She noted that the range for the 10-year bond yield is 3.75% to 4.50%, with short-term risks pushing rates higher, but longer-term, we’re already at the higher end of the range.

Meaning we’re already capped out factoring in all the stuff happening at the moment.

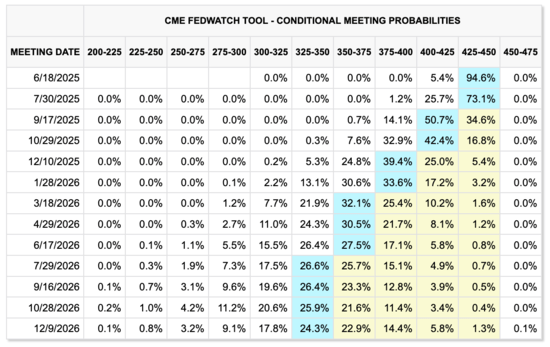

One of her biggest takeaways was that “The Fed is still in a neutral to easing bias.” There are no rate hikes on the table.

In fact, if you look at the CME FedWatch probability chart above, there is a 0.0% chance of a rate hike from now through the end of October 2026. And only a 0.1% chance by the end of 2026.

She added that some of the new government budget has already been priced in to the long end of the yield curve.

So it’s not like mortgage rates need to keep going up to compensate if it’s already baked in.

Remember, we were very close to a 6% 30-year fixed last September, and are now at 7.125% as of this writing.

Mortgage rates ARE already higher to compensate.

Meanwhile, the economy continues to show signs of weakness and ultimately the future of rates will depend on that very inflation and economic data.

That might explain why Fannie Mae’s latest projection released yesterday has the 30-year fixed falling to an even lower 6.1% by the end of 2025 and 5.8% in 2026.

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.