It’s been a good couple of weeks for mortgage rates during the ongoing government shutdown.

Historically, they tend to do well when the government isn’t operational. The short answer why is a perceived flight to safety (in bonds), which pushes interest rates lower.

The 30-year fixed is now at its lowest point in about three years, having fallen about 20 basis points (0.20%) since the shutdown got underway on October 1st.

At the same time, a dearth of new economic data from the government makes it hard for rates to do too much.

That changes tomorrow, when we get a (delayed) CPI report for the month of September.

CPI Report Has the Chance to Be a Big Mortgage Rate Mover Tomorrow

While the CPI report isn’t necessarily the biggest mover of mortgage rates, it does carry a good amount of weight.

Especially lately with inflation being top of mind these past couple years, due in part to the record low mortgage rates many enjoyed (and continue to enjoy).

I’d argue the monthly jobs report is the heavyweight, but that’s on hold until the government gets back to work.

The CPI report was too, but it turns out the Social Security Administration (SSA) needs it to calculate the Cost-of-Living Adjustment (COLA).

So it was produced by some government workers who got dragged back into work…

Since nothing else is coming down the pike in terms of new data, and because we’ve been in a data blackout for weeks, it’ll clearly matter more than it usually does.

The lack of additional data also means it could have staying power, as there won’t be another government report to refute it.

For example, if it comes in cool and shows slowing inflation, mortgage rates might get nudged ever closer to the 5% range.

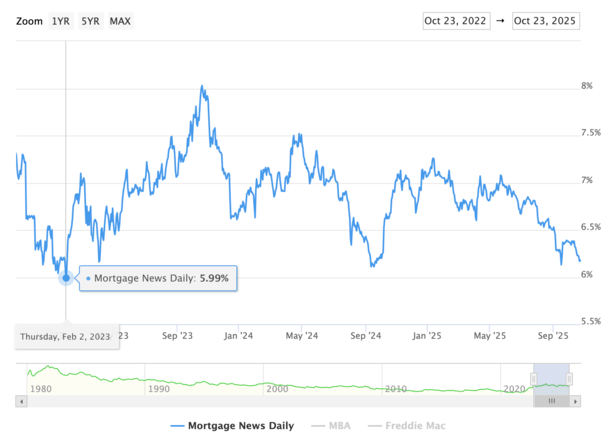

As seen in the chart above from MND, the 30-year fixed hasn’t been sub-6% since February 2023!

Conversely, if it happens to come in hot and we see that prices are on the rise again, it could send mortgage rates back toward the mid-6s.

Then you wouldn’t really have much to get them back to where they were until more data is released.

Long story short, it’s a potentially big report and all eyes will be on CPI tomorrow morning.

Mortgage Rates Playing Defense on Eve of the Report

Blame it on ongoing trade tensions between the U.S. and China, or perhaps some defensiveness ahead of tomorrow’s report, but the 10-year yield popped today.

It climbed about five basis points to get back above the key 4% threshold, which wasn’t necessarily enough to make mortgage rates go up today.

But it does show you that there’s some defense being played on the eve of the report. Nobody wants to stick their neck out before the lone government data report gets released.

That means mortgage lenders might also be hesitant to lower mortgage rates much more than they already have.

However, if that report comes in cold tomorrow, we might see another leg lower, ever closer to the key 5% threshold for the 30-year fixed.

It could be helped on by mortgage-backed securities (MBS) plumbing, where investors shift to lower-coupon buckets if they expect rates to come down further.

So there is the potential for this to serve as a sort of catalyst for rates that start with a 5.

Of course, it might also be an innocuous report that does little to nothing for rates. Or, as stated, it comes in hot and results in higher mortgage rates. Basically everything is on the table here.

And it could also sway what the Fed has to say at its meeting next week, before it’s next monetary policy decision.

For the record, they are widely expected to cut the federal funds rate another 25 bps next Wednesday, with CME odds currently at about 99%.

That likely won’t change regardless of this CPI report. But it could provide downward (or upward) momentum for mortgage rates depending on the outcome.

Read on: How to track mortgage rates with ease.

(photo: atramos)

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.