I know we just recently got a 5-handle for the 30-year fixed after several years in much higher territory.

But is it too soon to talk about 4% mortgage rates?

The reason I ask is because I’m seeing some aggressive rate quotes that are already nearly there.

So if we get some more favorable economic data and/or we hear more on proposals like the MBS buying, we could get the nudge needed to get them.

If it were to happen soon, during the traditional spring home buying season, it could be big.

The Return to 5% Mortgage Rates Took Years

At last glance, the 30-year fixed was averaging 6% on the nose, per the latest read from Mortgage News Daily.

It enjoyed two days at 5.99% before ticking up a single basis point, and chances are it will tick back down to 5.99% today.

Sure, it’s not a really a 5% mortgage rate, but a 5-handle mortgage rate.

In other words, it starts with a 5, but it’s far cry from 5%.

If it were 5%, there’d likely be a mad rush to buy homes again, though anecdotally I’m already hearing of bidding wars heating up again.

But here’s an important point. The rate indexes like MND’s simply represent composite mortgage rates for the market.

Put another way, a snapshot of the lender universe on any given day, mostly useful to track day-to-day movement as opposed to real rates.

This is to say that if their index says 5.99%, there are borrowers out there securing even lower rates (or in some cases higher rates).

One Big Bank Is Nearly in the 4% Range for a 30-Year Fixed

That brings me to a big bank I check in on from time to time, which just so happened to be offering rates super close the 4s.

Again, we’re talking a 4-handle, aka 4.99%, not a 4% mortgage rate. And again, if rates were 4%, it’d likely be a madhouse out there between surging refinance applications and bidding wars.

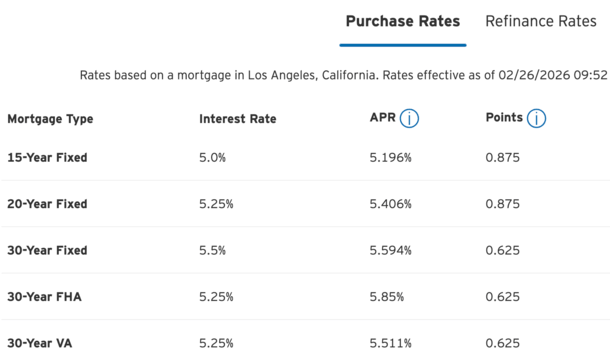

Instead, I’m seeing rate quotes of 5.25% for both FHA loans and VA loans (which are always the cheapest loan options), and 5.5% for a conforming loan (Fannie/Freddie) 30-year fixed.

They’re also advertising a 15-year fixed at 5% even, meaning just one basis point above the 4s. And a 20-year fixed at 5.25%, not far either.

In other words, almost into the 4s across a number of different loan programs.

So in reality, there are a lot of lower mortgage rate quotes swirling around, well below the national averages we see in the headlines.

Notably, none of these rates even require a massive buydown (discount points) to get the deal.

Lately, lenders have attempted to lure in borrowers with heavily bought-down rates that often require 1.5% to 2% in points.

That can be super expensive since one point costs $1,000 for every $100,000 in loan amount.

But these rates mostly require a fraction of discount points, whether it’s 0.625% or 0.875%.

Sure, it’s still not free, but it’s quite reasonable, especially if you can get seller concessions and use those for these closing costs.

4-Handle Mortgage Rates Would Be Big for the Housing Market Recovery

While we’re not quite there yet, the fact that some banks and lenders are already offering rates in the low-to-mid 5s is promising.

It means actual rate quotes and eventual rate locks will come in significantly lower than the national averages we see in the news.

This will make housing that much more affordable for prospective home buyers, while also giving more existing homeowners the opportunity to take advantage of a rate and term refinance.

If we continue to receive favorable economic data, such as lower inflation, or see more flights to safety (in bonds) as the stock market corrects, mortgage rates could move lower.

There are also pending initiatives like Fannie and Freddie’s $200 billion MBS buying program that could give rates a little push down as well.

And that could mean that some of these quotes that are already near the 4s could eventually get there.

So while everyone talks about 5% mortgage rates, it might not be unheard of to hear about borrowers snagging rates in the 4s again!

Just know that you’ll likely need a vanilla loan scenario, meaning an owner-occupied property, excellent credit score, low loan-to-value ratio (LTV), etc.

Read on: 2026 Mortgage Rate Predictions

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.