Well, the housing market appeared to be warming up in February, but it might prove to be temporary.

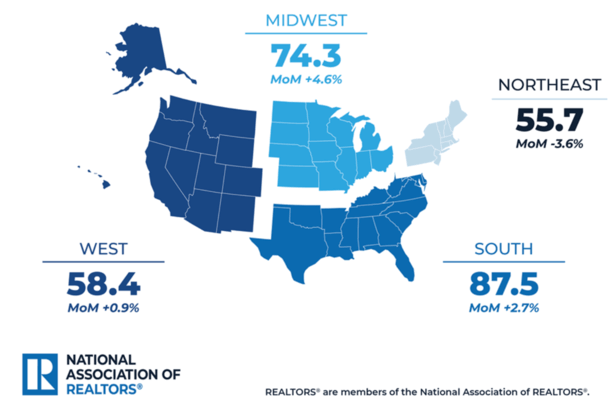

The National Association of Realtors reported that pending home sales unexpectedly rose 1.8% month-over-month versus a median forecast of -1%.

So aside from not being negative MoM, they also beat expectations, which is clearly a positive.

However, they were still down 0.8% year-over-year and the outlook isn’t great given mortgage rates hit 3.5-year lows in February.

Because as we all know, mortgage rates are a lot higher today than they were just a few weeks ago.

Pending Sales Went Positive in February, But It Might Not Last

Pending home sales are a forward-looking indicator as they represent signed contracts to purchase a home.

That means a pending home sale from February will likely close in March or April because it takes anywhere from 30-45 days to get a mortgage, if not longer.

So we’ll see a bump in existing home sales once these get to the finish line, assuming they all do.

But it doesn’t appear to be the big jump many were expecting this year, including NAR that projected a double-digit increase in home sales compared to 2025.

Given we were only able to muster a sub-2% increase in pending sales during a month in which mortgage rates hit 3.5-year lows tells you everything you need to know.

It’s not exactly a blockbuster number, despite beating the very low bar set by economists for the month.

Nor does it paint a particularly bright picture for the start of the spring home buying season.

Assuming mortgage rates stay elevated from now through at least summer, you can’t foresee sales getting much better.

The Mortgage Rate Spike Will Absolutely Slow Down Home Sales

The ongoing conflict in the Middle East, which began at the very end of February, has led to a big spike in oil prices.

The knock-on effect has been markedly higher mortgage rates, as higher oil prices leads to inflation, whether it’s elevated gas prices or higher input costs for the production and transportation of goods.

This led to a big jump in 10-year bond yields, which had been sub-4% prior to the conflict and looking to drop even more.

That was the reason the 30-year fixed mortgage was the lowest it had been since late summer 2022.

And given mortgage rates were still near all-time lows in early 2022, it was a pretty good place to be, especially in early spring.

Now the picture has changed tremendously, with mortgage rates rising from sub-6% levels to nearly 6.50% by some measures.

We have seen a slight reprieve this week, but it wouldn’t shock me to see mortgage rates move higher before they come down meaningfully.

In other words, there might be short windows to lock in a cheaper mortgage rate, but rates will remain significantly higher than levels seen at the end of February and early March.

The other issue is that the conflict has led to a stock market rout.

So you’ve got prospective home buyers grappling with higher mortgage rates while also looking at a depleted stock portfolio and simultaneously paying more at the pump.

The cumulative effect is consumer confidence will be lower, and as such fewer people will move forward with a home purchase.

That means 2026 could be yet another rough year for the housing market despite looking so bright just weeks ago.

Read on: 2026 Mortgage Rate Forecast

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.