So far this year, mortgage rates are behaving as they typically do.

They fell in the winter months and began rising in spring.

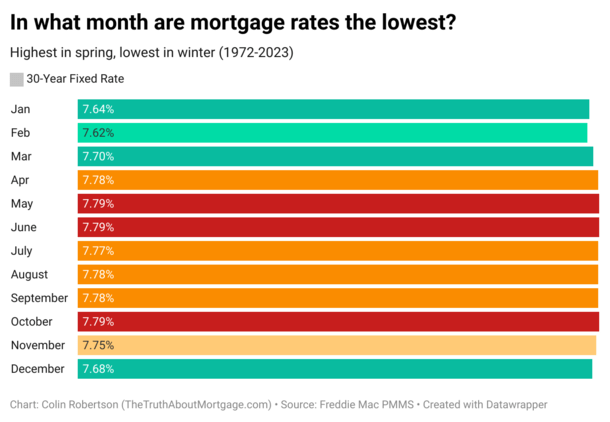

Right on schedule, the 30-year fixed hit a multi-year low in the month of February, which has been the best month for mortgage rates going back to 1972.

I did the research on this so I know. And like clockwork, they jumped in March and went even higher in April, despite having one good week recently.

The next logical question is do they move even higher in May and June, historically the worst months for mortgage rates on record?

Watch Out for Higher Mortgage Rates Next Month and Through Summer

As noted, I researched mortgage rate data going back to 1972, using Freddie Mac’s weekly mortgage rate survey.

I found that February was the best month for mortgage rates historically, though there are always exceptions to the rule.

Conversely, mortgage rates were found to be highest in the late spring and summer months, namely May and June.

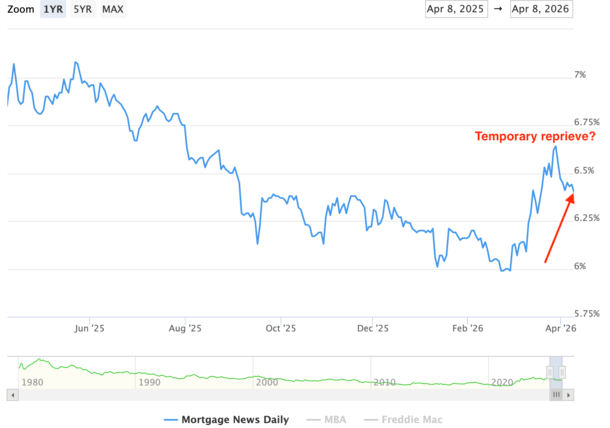

It’s nearly mid-April and mortgage rates are a lot higher than they were in February.

Back at the end of February, the 30-year fixed hit a 3.5-year low of about 5.98%, per Freddie Mac.

Then we got the unexpected conflict in the Middle East, which quickly sent mortgage rates flying.

Sure, nobody could have predicted that, but one way or another, trends always seem to present themselves.

At last glance, the 30-year fixed is averaging around 6.40%, so it’s up about a half point since those February lows.

Of course, it’s also down about 0.25% from the highs seen at the end of March when the 30-year fixed was closer to 6.625%.

I assumed rates would keep moving higher from there, possibly touching 6.75% and then 6.875%.

But as we all know, mortgage rates don’t move in the straight line, even if they’re trending in one direction, which appears to be UP right now.

This Could Be the Calm Before the Storm

Mortgage rates have gotten a slight reprieve lately, falling about 0.25% from recent highs, per MND’s daily index.

But it could be temporary, if we use historical data/trends as a guide, coupled with a really flimsy ceasefire in the Middle East.

After the ceasefire was announced Tuesday evening, we didn’t even go 24 hours, or even 12 hours, without more bombings and aggression in the region.

Then it was reported that the Strait of Hormuz was closed again, which seems to be the biggest issue for the global economy.

The fighting can continue, but if the Strait remains closed, oil prices will remain elevated near $100 per barrel and take that much longer to eventually normalize.

Assuming this happens, which is not at all far-fetched, chances are bond yields will rise again, inflation will rise, and mortgage rates will test new highs.

That’s where my prediction for a 30-year fixed at 6.75% or 6.875% comes in, perhaps in May and June.

It would be right on schedule, assuming we believe in historical mortgage rate trends.

And it would fit the narrative of things get worse before they get better.

But Mortgage Rates Could Still Fall Later in the Year

Since this conflict started, I’ve felt mortgage rates would go up, then eventually ease after late summer.

Those hoping the worst is behind us might be in for an unpleasant surprise.

It just doesn’t seem likely that given all that’s transpired, we can get back on our merry way and forget it all happened.

There will be lasting consequences, even if the tenuous ceasefire holds up, which it doesn’t look like it will.

In other words, more pain for mortgage rates for several months ahead, perhaps for the next six months.

But maybe just maybe you start to see improvement as the midterm elections become top of mind later in the year.

We know President Trump wants low mortgage rates. He campaigned on it and has talked about it repeatedly.

It will without a doubt be a goal to get rates lower. How he accomplishes that remains to be seen.

Even if he doesn’t have a direct hand in it, they might come another way. By way of recession…

Read on: Do mortgage rates go up or down during recessions?

(photo: Michael Coghlan)

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.