The defense sector is being repriced – and it’s not just about the war in Iran.

Allied budgets keep climbing across Europe and Asia. The Department of War is rewriting how it buys from its largest contractors. The market has reacted unevenly to all of it: Prime contractors get bid up on demand, sold off on execution risk, then bid up again on the next headline.

We evaluated one of them, Northrop Grumman (NYSE: NOC), last month. (Find out its score here.) Today, we’re looking at arguably its top competitor: Lockheed Martin (NYSE: LMT).

The company operates through four segments – Aeronautics, Missiles and Fire Control, Rotary and Mission Systems, and Space – and sells primarily to the U.S. government and allied nations through foreign military sales programs.

In fiscal 2025, Lockheed Martin reported sales of $75.0 billion, up 6% from $71.0 billion in 2024. Net earnings fell 6% from $5.3 billion, or $22.31 per share, to $5.0 billion, or $21.49 per share. The drop came from losses on classified programs and a one-time pension settlement charge.

Cash from operations reached $8.6 billion, and free cash flow came in at $6.9 billion. The order backlog – a tally of contracted work not yet delivered – hit a record $193.6 billion by year-end, up from $176.0 billion at the end of 2024.

The company returned $6.1 billion to shareholders: $3.1 billion in dividends and $3.0 billion in buybacks. Long-term debt stood at $20.5 billion (with just $1.2 billion coming due within the year), against $4.1 billion in cash on hand.

Lockheed Martin spent most of 2025 trading in a sideways band between roughly $420 and $510, well below the highs it had set the prior autumn.

Sentiment turned late in the year, however, and the stock ran from the mid-$450s to above $665 by March, briefly touching new highs. Since then, shares have given back more than $100 to trade near $554. That’s indicative of the market reassessing how much of the defense rally it was willing to fund at a premium.

That’s a wide round trip for a company whose underlying cash record barely shifted. The gap is worth examining.

The Value Meter framework is built to cut past the price swings and ask a simpler question: What does the business actually deliver, and how does the market’s price compare?

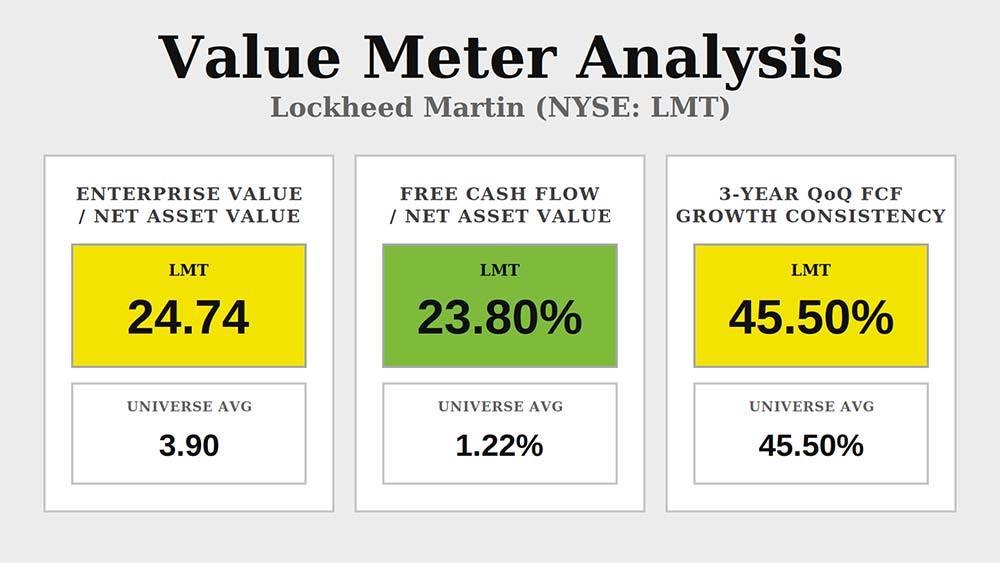

Lockheed Martin’s enterprise value-to-net asset value (EV/NAV) stands at 24.74, against a broad market average of 3.9. That is approximately 534% higher, meaning investors are paying a steep premium for every dollar of the company’s net assets.

Free cash flow-to-net asset value (FCF/NAV) sits at 23.80%, compared with 1.22% for the broad market. In other words, Lockheed throws off cash at nearly 19 times the market’s rate.

That productivity is what keeps the EV/NAV premium tethered to something real. For an investor buying today, the high price is funded by genuine cash output rather than assumed future growth.

Over the past three years, Lockheed Martin’s quarterly free cash flow has grown 45.5% of the time, exactly matching the broad market’s rate. That reflects the normal, milestone-driven rhythm of long-cycle defense contracting. At this valuation, that ordinary cadence doesn’t offer any extra margin of safety, but it doesn’t spell danger either.

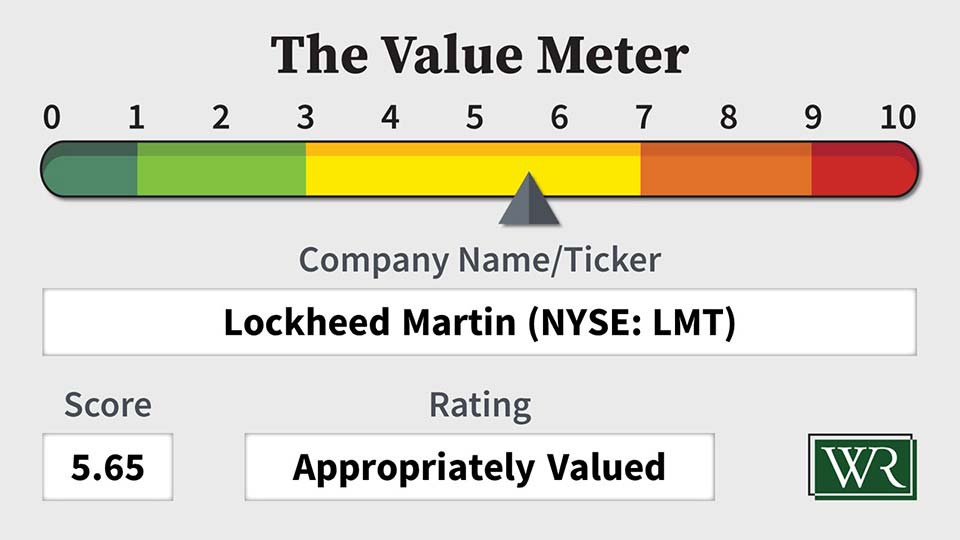

Read together, the metrics describe one pattern. The market is paying a steep price for Lockheed Martin, and it has a reason: The company generates cash at a rate few large companies can touch. What the market is not paying for is faster growth or smoother timing, and the record shows neither. Price and business quality are aligned.

The market prices Lockheed Martin as a premium cash generator without unusual growth credentials. The data backs that read.

The Value Meter rates Lockheed Martin as “Appropriately Valued.”

What stock would you like me to run through The Value Meter next? Post the ticker symbol(s) in the comments section below.