The recent surge in oil prices makes energy stocks look like a power play right now. But historically, they rarely enjoy the market’s full affection for long.

Oil prices move, sentiment swings, and investors start treating even the largest operators as if their earnings power might disappear overnight.

That backdrop has helped keep Shell (NYSE: SHEL) in a strange spot: It remains one of the world’s most important energy companies, yet its valuation still suggests a good deal of caution.

Shell is far more than a traditional oil major. It operates across upstream production, liquefied natural gas, fuels marketing, chemicals, and a growing portfolio of lower-carbon and power businesses.

That breadth matters. It gives the company multiple ways to generate cash, and it helps smooth out the pressure that can hit any one part of the energy market at a given time.

For the full year 2025, Shell reported revenue of $266.9 billion, adjusted earnings of $18.5 billion, and cash flow from operations of $42.9 billion. In the fourth quarter alone, revenue came in at $64.1 billion, adjusted earnings were $3.3 billion, and cash flow from operations was $9.4 billion.

Free cash flow for the quarter was $4.2 billion, and management guided to 2026 cash capital spending of $20 billion to $22 billion.

That sets up the core valuation question. Shell is still producing serious cash, but the market is not valuing those assets with much enthusiasm.

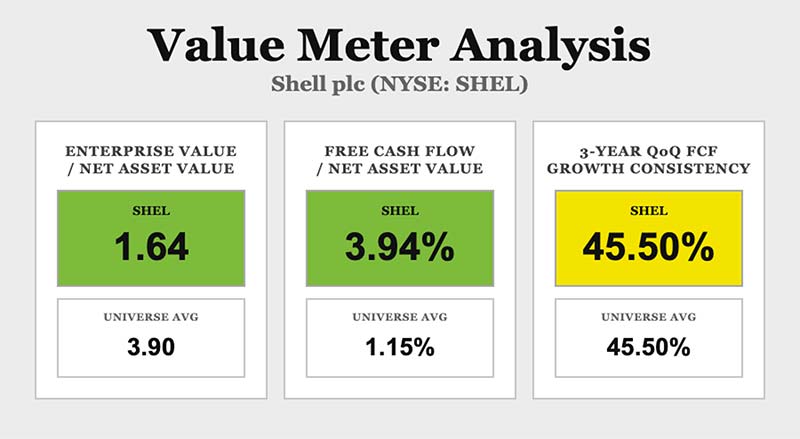

Shell’s EV/NAV ratio is 1.64, compared with a broad market average of 3.9. That means the stock trades at about a 58% discount to the broader market on an asset basis.

Investors are paying much less for each dollar of Shell’s net assets than they pay for the average company. That usually signals a market that is pricing in cyclical risk more heavily than current fundamentals.

The cash picture is stronger. Shell’s trailing free cash flow-to-net asset value percentage is 3.94%, versus a broad market average of 1.15%.

In plain terms, Shell is generating about 243% more cash from its asset base than the average company, which gives more support to the idea that the stock is trading at a discount.

Over the past three years, Shell’s quarter-over-quarter free cash flow growth consistency was 45.5%, exactly in line with the broad market average. Growth consistency is not giving investors an extra reason to pay up, but it is also not a weakness.

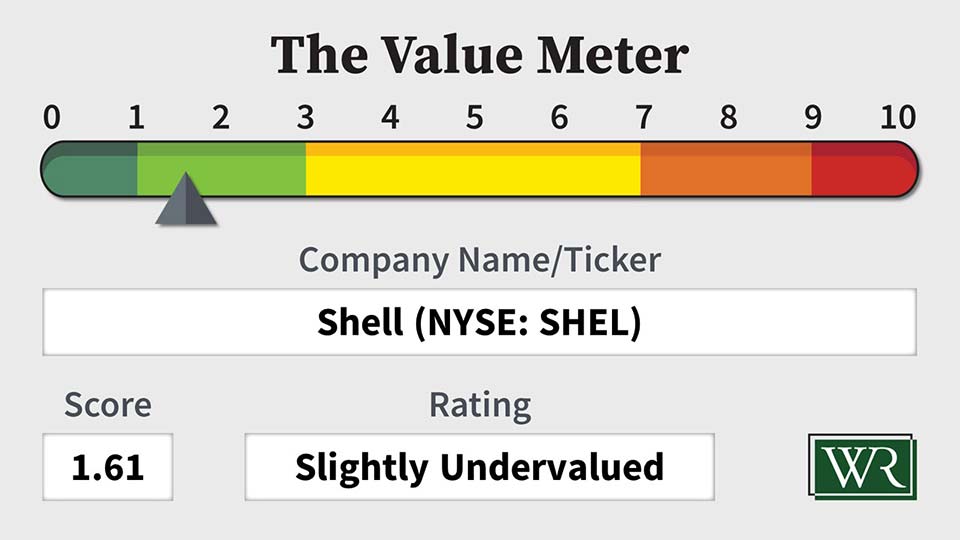

At first glance, Shell looks like another large, mature energy company that the market is content to keep on a leash. However, the numbers suggest something better than that.

Its asset valuation is low, its cash-efficiency is strong, and its growth consistency is perfectly serviceable. That combination does not point to a broken business. It points to a stock that still looks cheaper than it should.

The Value Meter rates Shell as “Slightly Undervalued.”

What stock would you like me to run through The Value Meter next? Post the ticker symbol(s) in the comments section below.