I keep hearing that more home buyers are considering adjustable-rate mortgages.

And you are seeing it in the data, with ARMs accounting for 8% of home loan applications, per the latest weekly read from the MBA.

It’s not a massive share, nor is it the fast and loose days of the early 2000s, but they are becoming more popular.

The issue though is interest rates on fixed-rate mortgages are also falling, so you need a decent discount to ensure the ARM is actually worth the risk.

This discount can vary widely by lender, often much more than it does for a 30-year fixed, meaning you need to put in the time to shop around.

ARM Rates Are Almost Into the 4s Again!

Whenever I want to see rates on adjustable-rate mortgages, I search local credit unions.

They tend to beat the competition because they offer more outside-the-box programs and are not-for-profit institutions.

This means they can offer lower rates to their customers instead of taking excess profits.

And because most nonbanks, which dominate the mortgage landscape today, stick to boring old 30-year fixed mortgages, they often aren’t very competitive when it comes to other products.

So if you’re considering an ARM, search some local credit unions in your city or state to see what they can offer.

You can still compare to the banks and nonbanks to be sure though!

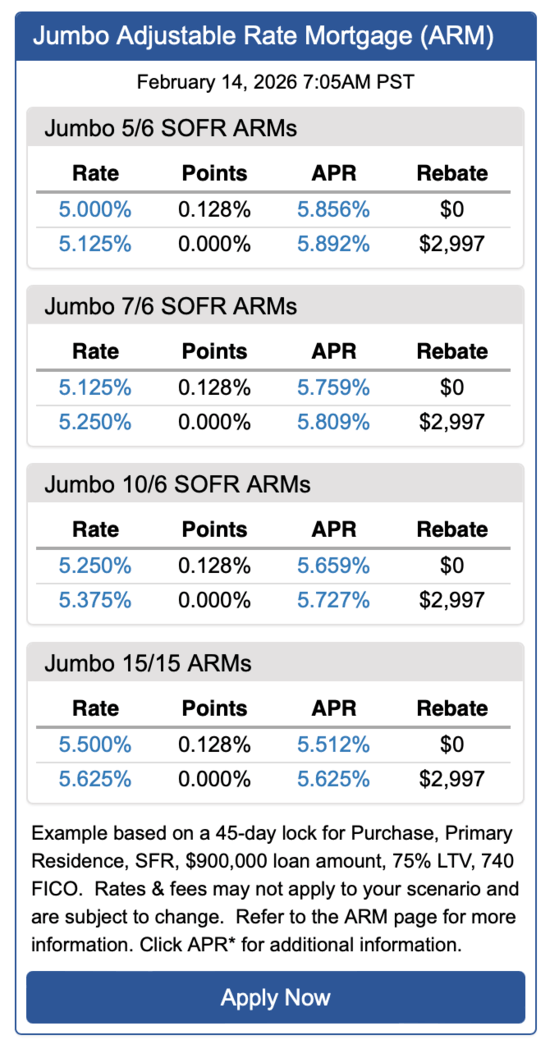

I did the same thing this morning and found one credit union offering a 5/6 ARM at 5% flat. And a 7/6 ARM for 5.125%.

Those were both with no points, required a 75% loan-to-value ratio (LTV), 740+ FICO score, and were jumbo loans.

Rates on conforming loans were about 0.25% higher, which might sound strange because often it’s the other way around.

My assumption is the credit unions want these bigger jumbo loans because they’re more profitable to keep on their books.

The customers may also have more assets they can park with the credit union, making them more attractive targets.

So if you’re buying an expensive home and in jumbo loan territory, the savings can be pretty substantial.

But even their conforming loans are pretty cheap relative to the 30-year fixed today.

What Do the Potential Savings of an ARM Look Like?

| $900k Loan Amount | 30-Year Fixed | 7/6 ARM |

| Interest rate | 6% | 5.125% |

| Payment | $5,395.95 | $4,900.38 |

| Savings | n/a | ~$500/mo. |

| Balance after 7 years | $789,951.19 | $774,935.21 |

Let’s compare a 30-year fixed at 6% versus a 7/6 ARM at 5.125% to illustrate the savings.

The credit union used a $900,000 loan amount so the principal and interest payment would be $4,900.38 versus $5,395.95.

That’s a monthly savings of nearly $500 per month or $6,000 per year. Not too shabby for a loan that is fixed for 84 months before its first adjustment.

Of course, you have to be prepared for an adjustment when you take out an ARM because it’s possible rates could be higher in seven years.

The good news is seven years is a long amount of time and it gives you optionality to refinance during that time without penalty, or sell the property if you choose.

It’s also possible to do nothing and hope the associated mortgage index is lower once the loan becomes adjustable.

That’s entirely possible if the Fed is looking to bring down short-term rates, which could translate to a lower SOFR, a popular mortgage index these days.

In other words, the ARM could be cheaper today and cheaper later, with no action required on the part of the homeowner.

One little extra bonus with the ARM is you’d pay down your loan balance a bit faster, so after seven years the balance would be roughly $775,000 versus $790,000 thanks to less interest charged.

Tip: If you’re looking for a HELOC, credit unions are also a good choice because they often don’t charge any fees nor require a minimum draw!

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.