Another fintech has been quietly growing in the mortgage space, looking to solve the age-old “buy before you sell” conundrum.

A major challenge for prospective move-up buyers these days is unloading their old property while securing a new residence.

Exacerbating the issue is a continued lack of for-sale inventory, coupled with waning affordability thanks to high home prices and mortgage rates.

This can make it difficult to float two mortgage payments while finding a buyer for their old home.

Enter Calque, which partners with local mortgage lenders to ensure the home loan piece is solved.

Calque’s Trade-In Mortgage

The Austin, Texas-based company actually offers two products to make it easier to buy and sell a home at the same time.

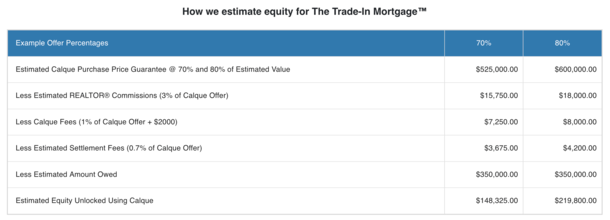

Their so-called “Trade-In Mortgage” allows home sellers to gain access to their home equity ahead of time without needing to sell first.

This second mortgage acts as a bridge loan, freeing up liquidity so you can make a stronger offer.

And it comes with a guaranteed back-up offer where Calque will buy your old home, allowing you to submit cash-like offers.

This gives buyers increased purchasing power in a number of different ways, whether it’s an increased down payment, larger cash reserves, or the ability to pay off other high-cost debt.

It can also make the buyer more competitive in a housing market that continues to be plagued by low inventory.

If you find yourself in a bidding war, coming in with a larger down payment can help you win the property over other bidders.

Even if competition isn’t strong, a larger down payment may allow you to make a low-bid offer, as the seller will favor an offer with more money down.

In addition, you can offset the cost of a higher mortgage rate on the replacement property by putting more money down.

A few months back, a friend of mine sold his old home with a super cheap mortgage and used the sales proceeds to pay down the new high-rate mortgage.

While this was a good solution to cut down on his interest expense, it didn’t lower his mortgage payments, which still amortize normally despite the extra payment.

This means he’ll either need to request a loan recast to lower future payments, or he’ll need to wait for a good opportunity to apply for a rate and term refinance.

The Trade-In Mortgage allows you to apply a larger payment on the new home upfront before you sell your old one.

As a result, you won’t necessarily need to refinance or complete a recast since lower monthly payments will be reflected by the smaller loan amount.

You may even be able to get a lower mortgage rate thanks to a lower loan-to-value ratio (LTV), and/or avoid private mortgage insurance (PMI) in the process.

And you can use some of the money from the bridge loan to fix up your old home so it sells for a better price!

Calque’s Contingency Buster

Recently, Calque rolled out a “lighter” buy before you sell option known as “Contingency Buster.”

It allows home buyers to achieve the same basic result without taking out a second mortgage.

In the process, they can make offers without home sale contingencies and exclude the old mortgage payment from their DTI ratio.

As long as your lender is approved to work with Calque, you can make a non-contingent offer on a new home while not worrying about having to qualify for two mortgages.

It’s hard enough to afford one mortgage, so attempting to float two at the moment is likely a deal-breaker for most.

Like the Trade-In Mortgage, Contingency Buster leverages the company’s Purchase Price Guarantee (PPG).

It’s a binding backup offer put in place that will only be employed if your current home doesn’t sell within 150 days.

The agreed-upon price will likely be below-market, with the sample calculator on their website displaying 70% or 80% of estimated value offer.

So obviously you’d still want to sell your home on the open market to a buyer other than Calque.

How Much Does Calque Cost?

There are three possible fees depending on which program you choose.

This includes a $2,000 flat fee paid to Calque, along with 1% of the Purchase Price Guarantee amount.

For example, if they offer to buy your old home for $600,000, it’d be $6,000 + $2,000, or $8,000 total, taken from your sales proceeds.

If you needed the bridge loan to access your equity ahead of time via the Trade-In Mortgage program, there’s also a $550 flat fee. And the interest rate is apparently 8.5% on that loan.

So you’d be paying some interest until you closed on the new home and were able to pay off the bridge loan with the proceeds.

Those simply using the Contingency Buster would only owe the $2,000 plus 1% of the offer price. This seems to be the case whether they sell the property on the open market or not.

Is This a Good Offer?

Whenever I come across programs like this, I try to determine if they’re a good deal or not.

Ultimately, many prospective home buyers can’t buy a new home without it being contingent on the sale of their old home.

It’s just impossible for a lot of folks to carry two mortgages from a qualification standpoint.

Even if they could, there’s also the uncertainty of the old home being stuck on the market and continuing to carry that cost.

So from that perspective, this alleviates those problems and concerns. But as noted, there are costs involved with the program.

And the biggest potential cost is selling your home for just 70% or 80% of its value. While the other fees are reasonable sounding, selling for a 20-30% haircut isn’t great.

In other words, Calque could be beneficial, but you’d still want to sell your old home to a third-party buyer for top dollar (or as close to it as possible).

Otherwise you could be leaving a ton of money on the table. And it kind of defeats the purpose of using the program to begin with.

For me, this means understanding upfront how easy it’d be to sell your current home and at what price to avoid any unwanted surprises.

Lastly, you’d need to use a mortgage lender who is approved to work with Calque. So you’ll also need to ensure this lender is competent and well-priced!

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 18 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on Twitter for hot takes.