Owning a home has several federal income tax advantages including the deductibility of mortgage interest and real estate taxes. Many homeowners may not be aware of the tax advantages associated with selling their home. This tax advantage is up to a $250,000 capital gains tax exclusion (up to $500,000 for a married couple filing jointly) if certain conditions are met.

While nationwide personal residential sales during 2025 were rather dismal, the residential real estate market has picked up somewhat in early spring 2026 especially average 30-year mortgage interest rates hovering around 6 percent. Older homeowners, particular those who retired in recent years and who want to sell their homes in recent years but could not, are anticipating some better times to sell their homes in 2026. This column discusses the IRS rules with respect to the sale of a principal residence. In particular, Internal Revenue Code (IRC) Section 121 regarding the $250,000/$500,000 capital gains tax exclusion from the sale of a principal residence.

What is the Primary or Principal Residence?

A primary or principal personal residence must be an individual’s main residence. This includes (1) House; (2) Houseboat; (3) Mobile home; or (4) Cooperative apartment or condominium. In IRS Revenue Ruling 54-611, the IRS said that the primary home or principal residence does not have to be in the United States.

Vacant land is not considered part of a main home unless the vacant land is: (1) Adjacent to the land containing the home, and (2) Used as part of the main home such as for recreation. If these two prerequisites are met, then the sale of the land and the sale of the home are treated as one sale.

Owning More Than One Principal Residence

Only the sale of the principal residence qualifies for the $250,000/$500,000 capital gains tax exclusion. Any other home sale is taxable. It is not possible to have two principal residences at the same time as the following examples illustrate:

Example 1. Aliza owns a home in Rockville, MD. She also owns a condominium in West Palm Beach, FL. which she uses during the winter months. The house in Rockville, MD is Aliza’s main home.

Example 2. Burton owns a home in Rockville, MD but he actually lives in Fort Lauderdale in a home he rents. The home in Ft. Lauderdale is Burton’s main home and the home in Rockville MD would not qualify for the $250,000/$500,000 capital gain exclusion.

For the purpose using the $250,000/$500,000 capital gains tax exclusion, Individuals who live in more than one home should use some basic facts to determine their principal residence. These factors include: (1) Place of employment; (2) Location of family members main home; (3) Mailing address; (4) Legal address for tax returns, driver’s license, voter registration, etc.; (5) Banking location; and (6) Location of clubs and houses of worship to which the individual belongs.

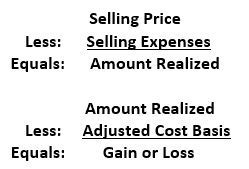

Determining Gain or Loss Upon the Sale of a Principal Residence

The formula to calculate the gain or loss upon the sale of principal residence is:

Note 1: The selling price does not include personal property such as furniture.

Note 2: The selling price does include mortgages or notes assumed by the buyer.

Note 3. Payments from employers to reimburse for a loss on a home sale are included on Form W-2 and should not be included as part of the selling price.

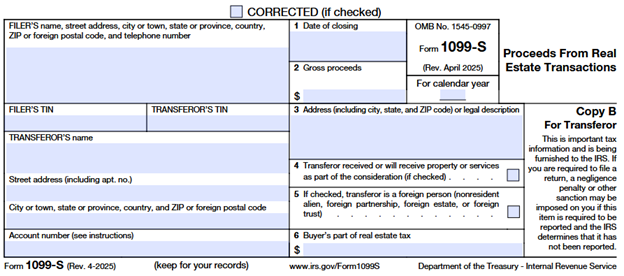

Note 4: IRS Form 1099-S (see below) is used to report the sales price. Some problems associated with Form 1099-S include: (1) The form does not include loan assumption or services rendered: and (2) The form may not be issued if the lender believes the entire sales price amount is excludable from federal income tax.

Note 5: Transfers to a spouse as a result of a divorce are not taxable or reportable.

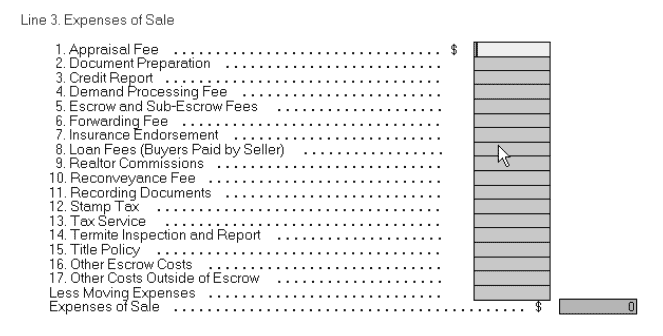

Note 6: Selling expenses include a number of items such as reprinted below from CFS Tax Tools software.

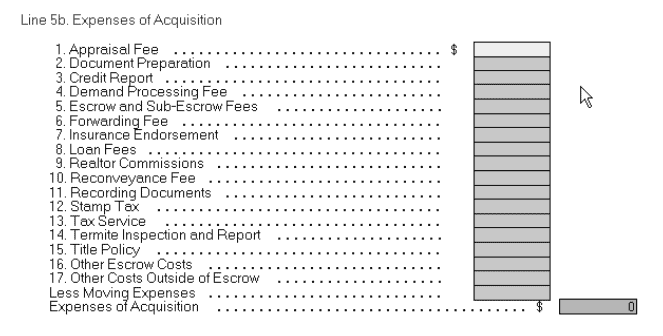

Note 7: Cost basis in a home is adjusted for a number of factors as reprinted below from CFS Tax Tools software.

Note 8: Losses on the sale of a principal residence are not deductible and cannot be applied against capital gain.

Note 9: On a married filing separate federal income tax return, each spouse’s gain or loss is calculated, and the applicable rules are applied separately according to ownership interest.

Note 10: In the case of a principal residence owned by unmarried individuals, each gain or loss is calculated and the applicable rules applied separately to ownership interest.

Three tests apply to a principal residence owner in order for the owner to exclude capital gain (profit) and tax resulting from the sale of a principal residence. The three tests are listed and explained:

• The ownership-test. The individual must have owned the residence for at least two years out of five years ending on the sale date.

• The use-test. The individual must have used the principal residences (lived there) for at least two years out of five years ending on the sale date; and

• The exclusion-test. The capital gain exclusion cannot be used more than once every two years.

The maximum amount of capital gain exclusion is $250,000 per individual. Note that in order to use the $250,000 capital gain exclusion, there is no requirement for the individual to purchase a more expensive principal residence. The capital gain exclusion can be sued more than once during an individual’s lifetime but not more than once every two years.

A married couple filing joint tax returns have a maximum capital exclusion of $500,000 and can be used if the following requirements are met:

• Either spouse must meet the ownership test.

• Both spouses must meet the use test (see above), and

• Neither spouse has excluded a capital gain exclusion resulting from the sale of a principal residence in the last two years.

Capital Gain Exclusion Resulting from the Sale of a Principal Residence Owned by a Surviving Spouse

As a result of the passage of the Mortgage Forgiveness Debt Relief Act of 2007, effective with tax years beginning on or after January 1, 2008, gain on the sale of a personal residence that had been jointly owned by a surviving spouse and his or her deceased spouse will qualify for the full $500,000 capital gain exclusion. This is only true if the sale closes no later than two (2) years after the date of death of the deceased spouse. Previously, the full exclusion was only available if the home was sold during the year that the spouse died.

Note the following:

• Either spouse may meet the ownership test but both spouses must meet the use test for this rule.

• If the surviving spouse remarried two years following the death of his or her deceased spouse, then the exclusion amount reverts back to $250,000, and

• Personal residences owned separately by the surviving spouse rather than jointly with the deceased will also qualify for this special treatment.