While it’s been said countless times, it bears repeating: the Fed doesn’t set mortgage rates.

The Fed simply sets short-term interest rates, driven by its dual mandate of price stability and maximum employment.

Nowhere on the Fed’s to-do list is ensuring mortgage rates remain attractive for home buyers.

It’d be nice, but it’s simply not the case. Instead, mortgage rates are driven by longer-term debt, namely the 10-year Treasury.

And the price/yield of the 10-year is dictated by economic data, which has continued to show strength, for now.

The Fed Will Hold Rates Steady Tomorrow

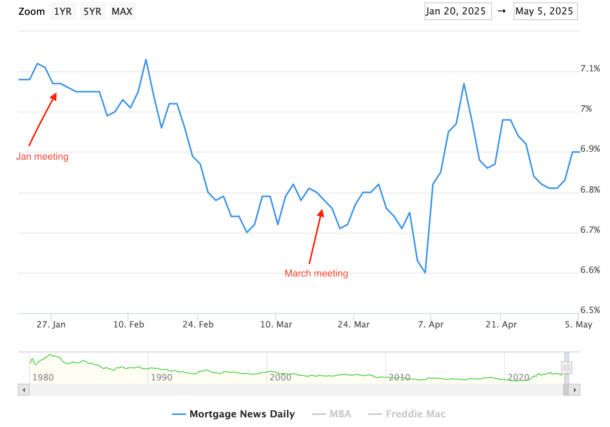

As seen in the chart above from MND, the last two Fed meetings had no impact on mortgage rates.

It’s basically a foregone conclusion that the Fed will hold its short-term fed funds rate steady again tomorrow at a range of 4.25% to 4.50%.

At last glance, the CME FedWatch Tool has odds of 96.8% for no action, meaning bonds and mortgage rates won’t be swayed (not that they necessarily would anyway with a cut/hike).

But the takeaway is there isn’t a compelling case at the moment for the Fed to take any action.

This means mortgage rates should also remain relatively flat for the foreseeable future, barring any new economic data that comes in overly hot or cold.

The last meaningful economic report was the monthly jobs report (NFP), which surprised on the upside and had many speaking to the resilience of the U.S. economy.

Some 177,000 jobs were added in April, significantly higher than the estimated 133,000 median forecast.

However, there are growing concerns of a recession, especially as the effects of the trade war begin to show up on Main Street.

There’s a theory that businesses are front-running tariffs, meaning business looks hot because they’re jamming in as much of it as possible before it gets more expensive.

But you talk to people on the street and things don’t look or feel so rosy.

So there’s a chance the data is lagging and might be painting an overly optimistic picture for an economy on the brink.

That would actually spell good news for mortgage rates, as bad economic news is often an effective way to lower interest rates.

Trump Again Asks for the Fed to Cut Rates Now!

On his Truth Social platform, Trump applauded the jobs report and argued that due to a lack of inflation, the Fed should lower rates.

As noted, even if they did, it likely wouldn’t lead to a lower 30-year fixed if economic data didn’t support it.

Ultimately, bond yields drive mortgage rates, and if those don’t come down, even if the Fed were to cut, mortgage rates won’t either.

The Fed, like bond traders, don’t appear to be in any rush and are in what feels like a perfectly appropriate holding pattern.

After all, there’s just too much uncertainty regarding the trade war and tariffs that has yet to show up in the data.

Making any major move when you don’t know the impact wouldn’t be prudent. We simply don’t know what this will look like, nor how long it will go on.

Or if the White House will strike a deal with China. That’s the one thing that could move rates more than anything else right now, perhaps.

With so many unknowns, and economic data arguably good enough to maintain the status quo, the Fed won’t cut.

The last Fed rate cut was on December 18th and the next one isn’t expected until July at this point.

That can change, but the takeaway recently is the expected Fed cuts have been pushed back.

There are still four quarter-point cuts projected by January, but until recently, four were expected during 2025.

Why I Expect Lower Mortgages in the Second Half of 2025

Simply put, lower mortgage rates have been delayed, as I kind of anticipated in my 2025 mortgage rate prediction post.

I always felt that the second quarter would see an uptick, as it normally does, before easing began in the third and fourth quarter.

This is especially true this year due to the trade war, and the next big shoe to drop is the proposed tax cuts, known as “one big, beautiful bill.”

While it’s supposed to help real wages for Americans and boost take-home pay, it’s also expected to significantly increase government spending and debt issuance along with it.

That’s slated to go down around Independence Day, so that too should limit what the Fed can do, while keeping bond traders in a tight range.

But as the economic data weakens, as many suspect it will, chances are bond yields will drop and mortgage rates will come down with them.

It’s probably a matter of when, not so much if, though if the tariffs prove to be inflationary (still unclear), that could dampen any improvement in rates.

The Fed will be watching these developments (and data) closely to determine its next move, but bonds will likely lead the way before they act.

So pay attention to upcoming jobs reports, the 10-year bond yield, and the price of MBS to track mortgage rates.

If the economic data points to a recession and/or slowing economic growth, the silver lining will be lower mortgage rates.

It might just take a bit longer to get there than originally expected if we see a temporary economic “boom” from front-running tariffs.

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.