We last looked at food maker General Mills (NYSE: GIS) in October.

At the time, the stock had a generous 4.9% yield. Today, the yield is 6.5% – and it’s not because the dividend has increased. The stock has been a disaster.

The 26% drop in the price of General Mills shares over the past six months has caused the yield to climb significantly higher. As a result, some investors may be willing to sit and wait while they collect that big dividend.

But is that dividend as reliable as a bowl of General Mills’ Cheerios?

In addition to the cereal that virtually every toddler in America has mushed into the couch, General Mills has many other household-name brands, like Betty Crocker, Cinnamon Toast Crunch, and Wheaties.

When I analyzed General Mills’ dividend safety in October, it received a “D” rating because free cash flow was falling.

The situation hasn’t gotten any better. In fact, it’s worse. It’s like expecting to be served Count Chocula and getting a heaping bowl of Raisin Nut Bran instead.

Folks just aren’t buying as much Green Giant, Lucky Charms, and Pillsbury as they used to. Revenue declined by half a billion dollars between fiscal 2023 and 2025. Wall Street expects sales to plummet even further from 2023’s peak of $20.1 billion to $18.4 billion in fiscal 2026 and to $18 billion in 2027.

That drop is hurting free cash flow, which is the lifeblood of dividends.

Companies need to generate cash in order to pay shareholders.

Earnings are nice, and they help to support a stock’s price. But earnings include all kinds of noncash items, such as depreciation. Dividends are not paid out of earnings, but out of cash flow.

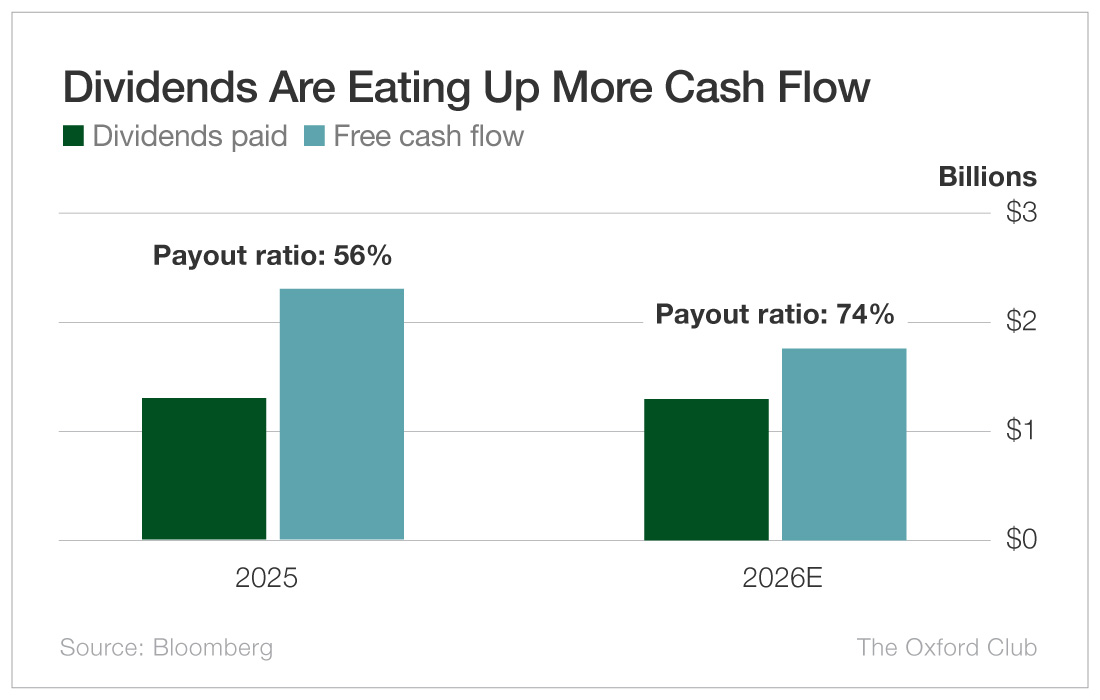

In 2025, free cash flow dropped from $2.5 billion to $2.3 billion. At the time I covered General Mills in October, free cash flow was forecast to decline to less than $2.2 billion in fiscal 2026. Today, that projection has fallen all the way to below $1.8 billion.

Last year, General Mills paid out 56.2% of its free cash flow in dividends. That’s fine. I’m good with anything below 75%.

This year, if the forecasts are correct, General Mills will be bumping right up against that threshold with a 74.1% payout ratio. It’s still okay, but it’s getting a bit close for comfort.

General Mills does have a good dividend-paying track record. It has paid shareholders a dividend for 128 years and has raised the dividend every year since 2021.

However, the drastically falling free cash flow means management may have some very tough decisions to make in the near future.

Falling free cash flow is a cardinal sin in the Safety Net model, and the model is not merciful when it comes to dividend safety grades. If a company’s free cash flow is falling and is not expected to get better, the dividend safety rating suffers mightily.

That is the case with General Mills.

Even though the company currently generates enough cash to pay the dividend, the rapidly deteriorating free cash flow means the dividend is not safe.

Dividend Safety Rating: F

What stock’s dividend safety would you like me to analyze next? Leave the ticker in the comments section.

You can also take a look to see whether we’ve written about your favorite stock recently. Just click on the word “Search” at the top right part of the Wealthy Retirement homepage, type in the company name, and hit “Enter.”

Also, keep in mind that Safety Net can analyze only individual stocks, not exchange-traded funds, mutual funds, or closed-end funds.

The post General Mills: Can This 6.5% Yielder Hang in There? appeared first on Wealthy Retirement.