The foreign tax credit is a federal tax credit used to offset income tax paid abroad. Generally speaking, US citizens pay income tax on their worldwide income. That income includes both incomes received within the US and outside of the US. If a US citizen pays tax to a foreign country on income earned in that country and, assuming the US. has a tax treaty with that foreign country, then the US citizen is entitled to a foreign tax credit. The foreign tax credit offsets tax paid to other countries; in particular, foreign taxes paid on income, wages, dividends, interest and royalties generally qualify for the foreign tax credit.

It is important to understand that a tax credit is a dollar-for-dollar reduction of the tax an individual owes, directly lowering an individual’s overall tax liability. Unlike an income tax deduction which reduces the amount of income subject to tax, credits directly reduce the final federal income tax liability.

Foreign Income Tax Deduction or Foreign Tax Credit?

Individuals who paid taxes to a foreign country on income generated or received in that country and who are subject to US tax on the same income may be eligible for either a foreign income tax deduction or a foreign tax credit.

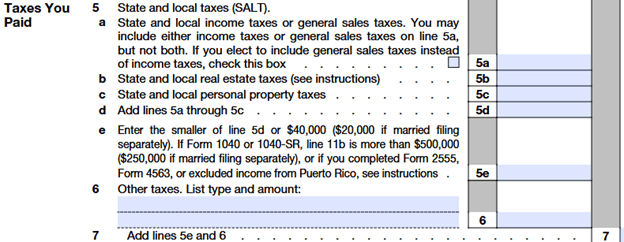

Those individuals who want to report foreign taxes paid as an income tax deduction may do so as an itemized deduction on IRS Form 1040 Schedule A (Taxes You Paid) Line 6 (“Other taxes”) as shown here:

Note again that the foreign tax deduction reduces an individual’s taxable income. However, if an individual does not have a sufficient amount of other itemized deductions including medical expenses, mortgage interest and charitable contributions thus resulting in the individual taking the standard deduction rather than itemizing, then the individual will have to use the foreign tax credit instead as discussed below.

The following foreign taxes do not qualify for the foreign tax deductions: (1) Taxes attributable to excluded income such as the Foreign Earned Income exclusion; (2) Taxes attributable to foreign countries designated by the Secretary of State as countries involved with internation terrorism or that have no diplomatic relations with the US.; (3) Taxes that would be refunded if the individual made a claim; and (4) Taxes that are returned to the individual as a subsidy.

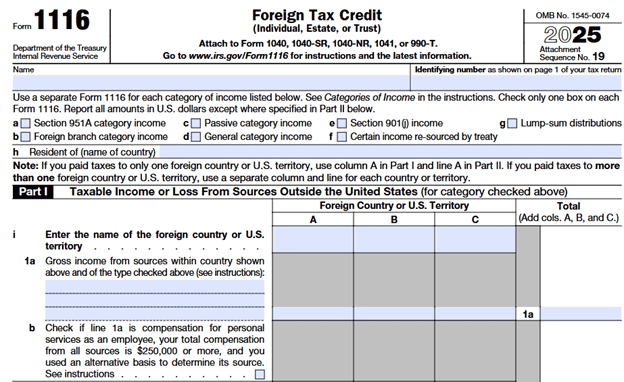

The foreign tax credit reduces an individual’s US tax liability “dollar for dollar.” Individuals who choose to take the foreign tax credit complete IRS Form 1116 (Foreign Tax Credit) (see below) and attach Form 1116 to their Form 1040 or Form 1040-SR. Taking the foreign tax credit usually makes more financial sense because the credit reduces an individual’s tax liability instead of just lowering the individual’s taxable income.

Qualifying for a Foreign Tax Credit

Not all taxes paid to a foreign government can be claimed by an individual as a foreign tax credit against US federal income tax. In order for the foreign tax to qualify for the credit: (1) The tax must be imposed on the individual by a foreign country or by a US possession; (2) The individual must have paid or accrued the tax to a foreign country or US possession; and (3) The tax must be the legal and an actual foreign tax liability the individual paid or accrued during the year.

Foreign income from wages, interest, dividends and royalties qualifies for the foreign tax credit. The IRS specifies that a foreign tax must be a levy and not a payment for a specific economic benefit. The foreign income tax must be similar to the US income tax. There is a limit on the amount of foreign tax credit an individual can claim. This limit is calculated on IRS Form 1116.

Note that an individual cannot claim both the foreign earned income exclusion and/or foreign housing exclusion and take a foreign tax credit for taxes on the income that the individual excluded or could have excluded. If an individual does claim both, the IRS could revoke one or both of the choices.

Refundable Versus Non-Refundable Tax Credits

A tax credit can be either refundable or non-refundable. A refundable tax credit results in the IRS paying a refund if the tax credit is more than an individual’s annual tax liability. For example, if an individual applies a refundable $4,000 tax credit to a $3,500 tax liability, then the individual will receive a $500 tax refund.

A non-refundable tax credit will not provide a refund because it only reduces the tax liability to $0. In the example above, if the $4,000 tax credit were non-refundable, then the individual would owe nothing to the IRS. But the individual would forfeit the $500 tax credit that remained after the credit was applied. Most IRS tax credits, including the foreign tax credit, are non-refundable.

US citizens and resident aliens pay federal income tax on their worldwide income no matter where they live. In order to avoid double taxation, the IRS allows a foreign tax credit for foreign taxes an individual pays or accrues. A nonresident alien can take the foreign tax credit if they were a bona fide resident of the US or Puerto Rico for the entire tax year and paid foreign income taxes connected to a trade or business in the U.S.