Lately, I’ve seen countless posts on social media from homeowners complaining that their escrow account is short.

And that their monthly housing payments will need to go up X dollars per month to cover the shortfall.

It’s either being driven by rising property taxes or higher insurance premiums. Or in some unfortunate cases, both!

To avoid this change in monthly mortgage payment, you can manage taxes and insurance on your own instead.

But how do you get rid of an existing escrow account?

Get Rid of Escrow on a Mortgage

- Escrow accounts ensure timely payment of taxes and insurance

- Often required when you take out a new home loan

- But can be removed if solid payment history and low LTV

- Fee is often charged (either flat fee or % of loan balance)

Many lenders require borrowers to open an escrow account when they take out a mortgage.

This is especially pertinent for those putting little down as it ensures the timely payment of property taxes and homeowners insurance.

Since both of these costs can be quite expensive, an escrow account ensures funds are collected monthly and distributed when the payments are due.

It’s all done automatically via the escrow account so the loan servicer doesn’t need to worry about a homeowner forgetting to pay.

If you’ve ever heard the acronym PITI, it stands for principal, interest, taxes, and insurance.

When you have an escrow account, you pay all four components each month, and then the T&I are disbursed when due.

If you don’t have an escrow account, you simply pay the P&I each month to your loan servicer, and self-manage the T&I portion.

But what if you want to get rid of your escrow account and self-manage? Well, it depends on your servicer and also your loan type.

You Might Have to Pay a Fee to Remove an Escrow Account

Some loan servicers will charge you a fee to remove an escrow account.

This could be a flat fee, such as $250, or alternatively a percentage of the outstanding loan balance.

Either way, it’s often not free. And if you try to waive impounds (different name for escrow) when obtaining a home loan, you may also have to pay a small fee as well.

This could be something like .125% of the loan amount, or $625 on a $500,000 loan.

The reason there is often a fee is because it’s lower risk to have an escrow account in place.

As noted, it ensures timely payment of taxes and insurance. Imagine if someone didn’t set aside the necessary funds, or forgot to pay, etc.

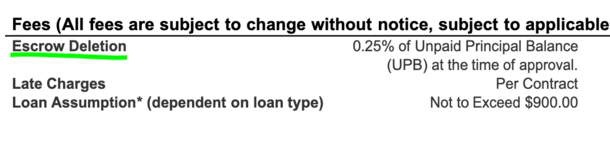

To determine how much it will cost you to remove escrows after you have your loan, find your latest mortgage statement and scroll down into the fine print area.

You should see something about “Escrow Deletion” or similar. One of my particular lenders charges 0.25% of the unpaid principal balance (see above).

So if you’ve got $200,000 remaining on your mortgage, that’d be $500! At that point, you’d probably say it’s not worth it.

After all, what’s the upside to self-managing these payments? You might be able to earn a little extra interest in a high-yield savings account?

But this can vary by loan servicer and even by state. Also note that you need to have a solid payment history and typically a low loan-to-value ratio (LTV) such as sub-80% or better.

The company may then review your loan and determine if you’re eligible to close the escrow account.

Tip: An escrow account is required on FHA loans for the life of the loan and can’t be removed. Same goes for USDA loans and while not a mandate for VA loans, most lenders still require it.

Why a Mortgage Escrow Account Is a Good Thing

Now before you get upset that you have to pay a fee to remove escrows, or find out they can’t be removed at all, consider this.

The timely payment of property taxes and homeowners insurance is clearly a good thing.

And taking a little out each month and paying it on your behalf ensures you won’t miss these crucial payments.

It also acts as a self-budgeting tool where you don’t have to worry about these big payments annually or semi-annually.

Instead, the loan servicer will not only budget for you, but also take care of the remittance.

We all know it can be hard to budget, so while it might be “annoying” to have to pay into your escrow account monthly, it can actually help you avoid bigger problems.

I personally don’t mind paying into an escrow account as it helps me avoid the shock of a big property tax bill or insurance premium.

In addition, the loan servicer will perform an escrow analysis each year and earmark additional funds if necessary to cover any expected increase (escrow shortage).

Sure, your mortgage payment will go up as a result, but it could be better than getting a surprise right before these payments are due!

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.