So I’ve had this article idea on my desktop since November 2024. It was an empty Word document simply titled “LLPA-free refinance.”

It was something I was thinking about for a long time because often a rate and term refinance won’t pencil (make sense financially) unless there’s a certain interest rate discount.

For example, if you can only lower your current mortgage rate by say 0.25% or 0.50%, there’s a decent chance it won’t make sense.

One of the issues with conventional loan (Fannie/Freddie) refinances is they’re subject to loan-level price adjustments (LLPA), which can result in a rate much higher than the par rate.

As such, what could have been a good loan that lowers an existing homeowner’s monthly payment is never pursued. Soon that may change…

LLPA-Free Refinance Could Ease Mortgage Payments and Lower Default Risk

Enter the LLPA-free refinance, which I’ve pondered since the affordability crisis took hold and mortgage rates nearly tripled.

Once they began to ease, there was a good opportunity for recent home buyers to lower their rates and get some payment relief.

Doing so would also result in lower default risks as a lower payment generally means the loan is more affordable and likelier to perform.

Despite that, rate and term refinances are subject to lots of pricing hits, the biggest being for credit score.

Importantly, these LLPAs apply to loans backed by Fannie Mae and Freddie Mac, but not on government mortgages such as FHA loans, VA loans, and USDA loans.

Because these fees exist, a recent home buyer might not be able to take advantage of the lower rates on offer without being subject to costly adjustments.

The end result might be passing on the refinance opportunity because it just doesn’t make sense financially.

How Much Could Borrowers Save Without LLPAs on a Rate and Term Refinance?

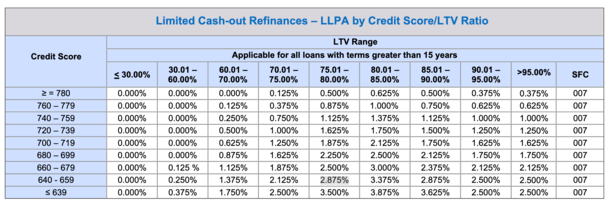

Let’s consider an example. A recent home buyer with a 690 FICO score would be subject to a 2.25% pricing hit for credit score at 80% loan-to-value ratio (LTV).

While it can vary, 1% in fee might equate to something like 0.25% to 0.375% in rate.

In other words, if their rate with the fee was 6.375%, perhaps it could be 6% without the fee.

And remember, all a rate and term refinance does (barring a product change) is lower the monthly payment.

So such a borrower would be turning in a riskier loan for a lower-risk loan by way of a lower monthly payment.

That should be appealing to Fannie Mae and Freddie Mac and investors too, who may assume the loan will be held longer and not prepaid quickly.

Instead, because the LLPAs do apply, the borrower might be told the best they can get is 6.375%.

If their existing rate is 6.875% or 7%, they may determine that it’s just not worth it to refinance.

LLPAs Waived on Home Purchase Loan But Not on the Refi

Making matters worse is some home buyers get their LLPAs completely waived for a home purchase loan, but they aren’t waived for a subsequent refinance.

As such, it’s even more difficult to get the refinance to pencil and make sense for the borrower.

They’re basically incentivized on the home purchase, but then kind of stuck in the loan, even if mortgage rates improve.

There are also those with lower FICO scores who are subject to massive LLPAs, despite only wanting to lower their payment and get some relief.

For example, a borrower with a 650 FICO at 80% LTV would be hit with a 2.875% fee.

If we translate that fee into rate, it might equate to 0.75% or more. So instead of 6%, they might be told 6.75% is the best they can get.

Again, if their current interest rate is 7%, chances are they won’t pursue the 6.75% rate.

But if they could avoid that big pricing hit and get the 6% rate, all of a sudden we’re talking some healthy savings.

On a $500,000 loan amount, a rate of 6% would be $2,997.75 per month vs. a monthly payment of $3,326.51 for a rate of 7%.

That’s roughly $330 in savings per month if the borrower can get the LLPA-free refinance.

And again, that’s a safer loan for all involved because the homeowner is paying $330 less per month.

It’s a Common Sense Idea That Could Lower Mortgage Rates Without Intervention

It seems like a pretty common sense idea to make the housing market safer and protect it from mortgage delinquencies and eventual foreclosure.

The good news is America’s Credit Unions, the Independent Community Bankers of America, and the Mortgage Bankers Association have all put forth such an idea this week.

In a letter to Kevin Hassett, the director of the National Economic Council of the United States, they appealed for this change.

The one caveat is you’d need an existing GSE-loan (backed by Fannie Mae or Freddie Mac) and a “strong payment history,” which they defined as no late payments in the past 12 or 18 months.

In the same letter, they called for “modestly lowering LLPAs across-the-grid for purchase loans” as well.

This could make home buying cheaper too and get mortgage rates lower without the need for MBS buying or lower bond yields or more QE and Fed intervention.

It actually makes a lot of sense to me so hopefully it’s something they’ll consider.

It’d definitely lead to a surge in refinance applications and lots of savings for American homeowners.

Read on: How does mortgage refinancing work?

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.