By now you’ve likely heard of mortgage rate lock-in.

It’s the theory that homeowners won’t move if they have mortgage rates well below prevailing market rates.

For example, a homeowner with a sub-3% mortgage rate is less likely to sell, all else equal, if rates are currently 6%.

And guess what? That’s exactly the current dynamic.

However, over time this naturally eases because despite lock-in, people still need/want to sell their homes for X, Y, and Z reasons.

Lock-In Easing But Still a Major Factor in the Housing Market

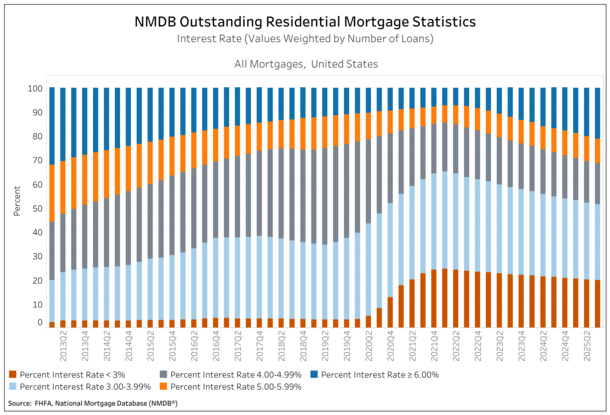

New data from the third quarter of 2025 has revealed that the share of outstanding mortgages with a rate above 6% exceeded those with a rate below 3% for the second straight quarter.

This is according to the FHFA’s National Mortgage Database (NMDB). This gap has also widened quite a bit since late 2022.

Only 7.3% of borrowers had a 6%+ mortgage rate in the second quarter of 2022 versus 21.2% as of the end of Q3 2025.

Meanwhile, the share with a sub-3% mortgage has fallen from a peak of 24.6% in the first quarter of 2022 to 20% as of Q3 2025.

So you can see that progress is being made on this front, but that it remains quite elevated.

Sure, we can celebrate the fact that the average outstanding mortgage rate is rising, thereby reducing the effect of mortgage rate lock-in.

But we can just as easily say 20% of outstanding mortgage loans are still priced at below 3%.

And chances are a lot of them have no intention of moving anytime soon, either because they can’t afford to or because they don’t WANT to give up their ultra-low rate mortgage.

Some critics of mortgage rate lock-in point to home sales still totaling about four million annually.

And sure, home sales still happen and transactions still exist, but you wonder where they’d be without this mortgage rate disparity.

There’s a reason existing homes sales have been hovering around a 30-year low lately…

Locked-In Homeowners = Less For-Sale Inventory, Higher Prices

It’s no secret housing affordability has been horrendous for years. Particularly since mid-2022 when mortgage rates quickly shot up from sub-3% levels to 7%.

And one of the reasons it’s been kind of stuck, with no major pullback in home prices in response, has been due to this lock-in.

Ultimately, if fewer existing homeowners are willing or able to move, they won’t list their properties.

This keeps a lid on for-sale supply and the old adage of supply and demand does its thing.

With fewer homes on the market, prices can remain elevated and affordability poor, even if there are fewer home buyers as well.

The result has been mostly flat prices for a few years, which is generally good news because it allows purchasing power to catch up over time.

And now that mortgage rates have fallen to 3-year lows, affordability has indeed improved.

We’ve got a combination of lower rates and flat (or even down prices) over a period of three years. That’s great for the housing market!

In addition, with the gap between prevailing market rates and outstanding mortgage rates shrinking as well, we should see more sellers come to market.

That will unlock more of this inventory that is badly needed in many markets nationwide and lead to higher home sales.

It could also lead to lower home price appreciation if there’s more supply to choose from, even if it’s cheaper.

I’m Never Selling This House!

While we’ve made some inroads on the lock-in effect these past few years, it’s not going to disappear overnight.

There are still countless homeowners out there who say, “I’m never selling this house.”

And they say that because of the low interest rate. As noted, some 20% of outstanding mortgage loans are still sub-3%.

Not to mention another 31.5% are in the 3.00% to 3.99% range, which collectively totals more than half of the market.

There are also a lot of loans in the 4.00% to 4.99% cohort, so it’s not going to correct itself as quickly as some think.

Certain markets will unlock faster than others too. I dug into the data a while back and found states like California were unlocking more slowly than other states.

So chances are for-sale inventory will continue to be constrained, even if more sellers come to market this year and beyond.

That’s probably a good thing though because it prevents a flood of inventory and big price drops.

When it comes down it, slow and steady improvement in affordability is the best way out of this mess. It’s just going to take time!

Read on: 2026 Mortgage Rate Predictions

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.