I wanted to wait until today to weigh in on the new plan for Fannie Mae and Freddie Mac to purchase MBS to see where the chips fell.

And it looks like what I expected, an improvement of .125% to .25% in 30-year fixed mortgage rates thus far.

Trump announced yesterday on his Truth Social account that he instructed Fannie and Freddie to buy $200 billion worth of MBS.

The move is intended to lower consumer mortgage rates, and shortly after that post, FHFA director Bill Pulte responded on X, saying “On it.”

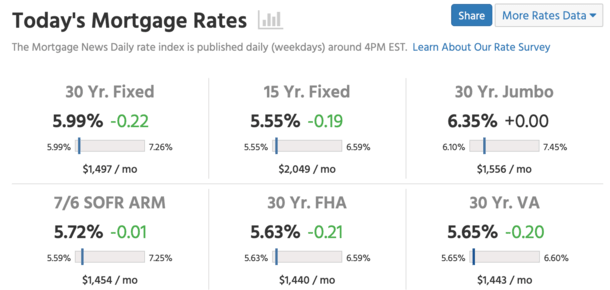

Today, we have a 5.99% mortgage rate, per the latest read from Mortgage News Daily.

This will be welcome news to just about everyone. The question is will rates continue to move lower, or is it a one-time shot in the arm?

Trump Admin Gets Its Sought-After 5% Mortgage Rate Headline

I found it interesting to see MND peg the 30-year fixed right under 6%, at 5.99% today.

That’s a big psychological victory for the Trump administration, as something like 6.01% wouldn’t have nearly the same impact.

It means they can say they lowered mortgage rates to 5% again after they surged to 8% under Biden.

Politics aside, it means more existing homeowners will be able to lower their mortgage rate via a rate and term refinance.

And more prospective home buyers will be able to qualify for a mortgage thanks to a lower monthly payment.

The start of 2026 was already looking pretty bright before this news, and now it’s that little bit brighter.

I had predicted a sub-6% mortgage rate by the first quarter in my 2026 mortgage rate predictions post, and it appears to have come even earlier than expected.

The next big question is how the housing market responds. I’ve said for some time that mortgage rates and home prices aren’t well correlated.

In other words, they can both fall together, rise together, or go in separate directions.

So don’t just assume home prices are going to surge again because mortgage rates are falling.

A 30-year fixed priced in the high or perhaps mid-5s is actually a nice sweet spot where affordability is better, but not all of a sudden a massive bargain.

This should increase home buyer demand without it turning into a frenzy, while also pushing more would-be sellers to list their properties.

Ideally, this results in a nice balance of buyers and sellers and more inventory to choose from, without the bidding wars and over-asking prices.

Big Banks Lowered Their Rates .125% Overnight

I’ve been talking to mortgage brokers and loan officers today to see what happened with rates overnight.

As I suspected, the improvement has been around .125% better, despite MND saying about .25%.

It will depend on the bank and lender in question, but my sources said pricing got better by about .50%, which translates to roughly .125% lower in rate.

I also looked at three major banks I’ve been tracking lately and they all improved by .125%.

This is what that looks like:

– Was 5.99%, now 5.875%

– Was 5.625%, now 5.50%

– Was 6.125%, now 6.00%

So one of the big banks is still quoting a 6%+ rate, while the others that were already sub-6% have moved a little deeper into the 5% range.

Ideally, this can get us a foothold in the 5s so we don’t just snap back to the 6s again, similar to last year when we kept creeping back toward the 7s.

If there’s more liquidity in lower MBS buckets, lenders will be able to offer more mortgages in the 5s moving forward.

It is a positive development for the housing market, but it’s not a return to 3% mortgage rates.

This is not another round of QE, where the Federal Reserve purchased trillions in mortgage-backed securities and long-dated Treasuries.

It’s a move to absorb MBS to improve pricing and lower mortgage rates for consumers via spread compression.

In other words, the 10-year bond yield can stay flat and mortgage rates can still improve thanks to this order.

Importantly though, the effects will be far more muted without improvement in bond yields.

Still Pay Attention to Economic Data If You Want Significantly Lower Mortgage Rates

If you want to see much lower mortgage rates (who doesn’t?), you’re still going to need additional weak jobs reports and more lower inflation reports.

Speaking of, we got the December jobs report this morning and it was kind of a mixed bag, thanks to job creation falling short of expectations (50k vs. 73k), but the unemployment rate dipping to 4.4% from 4.5%.

That resulted in flat bond yields today, but didn’t get in the way of this new MBS buying news either.

If the labor market continues to weaken and inflation continues to cool, we could see the 10-year bond yield fall as well.

Coupled with the MBS buying, you could envision mortgage rates falling closer to 5.5% and beyond.

The result would be more quotes in the high-4s assuming borrowers paid discount points at closing. Surely that’d be enough to fix the mortgage rate problem.

But there’s no guarantee that happens, so keep an eye on the data as it’s released and be vigilant if you’re considering a rate lock.

Conditions can change quickly.

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.