While 2026 started off well for mortgage rates, it’s beginning to feel more and more like 2025.

The reason why is tariffs.

For a very brief moment on January 12th, the 30-year fixed mortgage fell below 6%, averaging 5.99% per Optimal Blue and Mortgage News Daily.

It was driven by the news that Fannie and Freddie would buy $200 billion in mortgage-backed securities.

But it proved to be a very short-lived win after tariff talk entered the chat again.

New Korean Tariffs Put Mortgage Rates at Risk of Moving Higher

While we can argue about the effects of tariffs ad naseum, the clear takeaway is mortgage rates don’t like them.

So whether they cause inflation or not (they seem to by the way), it doesn’t matter if we’re discussing mortgage rates.

They aren’t good for rates and as a result prospective home buyers are effectively punished.

Existing homeowner get hurt too because a possible refinance gets pushed further and further away as rates drift higher.

The big reversal in rates took place just a week after the big drop, with the Greenland issue leading to a new round of tariffs on key European countries.

That felt very reminiscent of 2025 when it was tariffs, tariffs, tariffs to start the year.

While the tariff talk settled down as the year went on, it seems to have gotten a new life in the New Year.

And that means higher mortgage rates, all else equal.

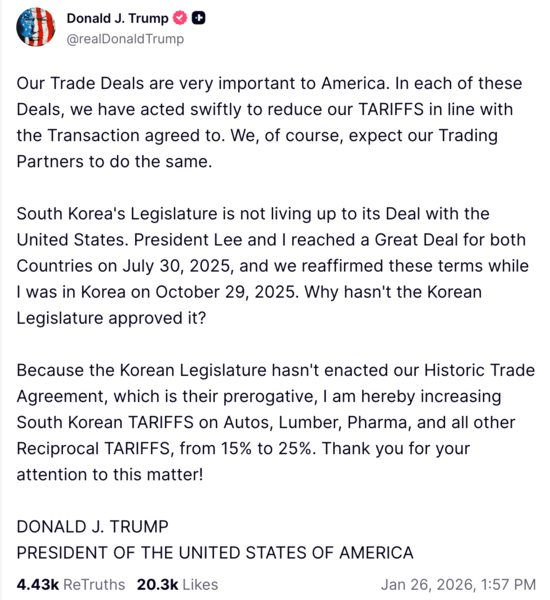

Today, Trump announced he was increasing tariffs on Korean automobiles, lumber, and pharmaceuticals to a rate of 25% from 15%.

The reason why was their failure to enact “our Historic Trade Agreement.”

Long story short, it’s more of the same stuff that will likely lead to higher bond yields and thus higher 30-year fixed mortgage rates.

Mortgage Rates Need a Catalyst to Move Lower

Since the Greenland debacle got started a week ago, the 30-year fixed has hovered around 6.20%.

It’s basically up .25% from the lowest levels seen post-MBS buying news and has been stuck ever since.

Yes, it has drifted down a few basis points, per Mortgage News Daily, but it’s been painfully slow.

The 30-year fixed has basically fallen at a rate of one basis point per day for several years, going from 6.21% to 6.17% at last glance.

In other words, rates are essentially flat and stuck, despite not worsening I suppose.

However, the slow trend downward last week could be completely erased if this new Korean tariff threat rattles the markets again.

There’s a decent chance it will and what little improvement was gained last week will be erased.

And without another catalyst to bring down rates, such as markedly improved inflation or another ugly jobs report, we might be stuck here (or even higher!).

If You’re Watching Mortgage Rates, Watch Out for More Tariffs!

I’ve been warning folks since the Greenland thing that the tariff talks usually rear their ugly head more than once.

So even if Trump backs off, there’s nothing to stop him from a second or third round of threats.

For example, it wouldn’t shock me to hear the Greenland (European) tariffs are back on the table at some point.

In the meantime, mortgage rates (and by extension home buyers) suffer the consequences of the unknown.

Long story short, banks and lenders will be hesitant to drop their mortgage rates by any sizable measure if there’s continued uncertainty.

Perhaps those 2026 mortgage rate predictions calling for flat rates throughout the year could ring true.

It’s a real shame too because the housing market was looking the brightest it has looked in years prior to these developments.

Read on: How to track mortgage rates with ease.

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.