In a bid to drum up excitement for its new mortgage offering, Opendoor will apparently offer below-market mortgage rates to home buyers.

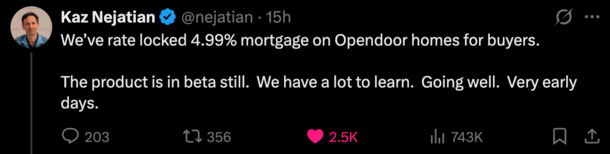

Per an X post, Opendoor CEO Kaz Nejatian said they would offer a 4.99% 30-year fixed mortgage with no points or fees.

That represents about a one percentage point discount relative to prevailing market rates, currently averaging closer to 6%.

The low rate is achieved via reduced margin, improved efficiencies, and scale.

The company recently announced that their mortgage product was in “beta” so it’s unclear when this will actually launch.

Opendoor Wants to Solve the Mortgage Rate Hurdle for Homeowners

CEO Kaz Nejatian has been rapidly launching new products in an effort to turns things around at struggling Opendoor.

The company is one of the original iBuyers, which allow people to buy and sell a home without a real estate agent.

Instead, they can sell their home to the company as-is, without all the usual hoops. And home buyers can purchase a home directly from the company as well.

The business model has never really taken off, in spite of being around during one of the hottest housing markets in decades.

It has since turned to a buyer’s market and remains unclear if that’s advantageous to Opendoor or will result in more of the same struggles.

Regardless, Nejatian (formerly of Shopify fame) is working feverishly to make the company a tech-forward, one-stop shop for home buyers and sellers.

Part of this strategy is reintroducing home loans, which were previously offered via Opendoor Home Loans but shuttered in late 2022 when mortgage rates surged higher.

In the X post, he went on to say that “we are committed to solving this for American homeowners.”

Of course, mortgage is a complicated business and this type of thing is easier said than done.

No Points. No Fees. 30-Year Fixed at 4.99%!

Nejatian did a bit of a Q&A session on X, which I appreciate transparency-wise, though it was somewhat light on details.

Regarding the cost savings, he said “Opendoor as the seller of the home has unique cost structures that allow us to do things.”

That means there’s a good chance they’re taking a page out of the home builders’ book and using a forward commitment.

This is where you buy a chunk of mortgages at a bought-down interest rate that aren’t tied to any one property or borrower.

Think of a car lease special where they say it’s $299 per month and there are five vehicles available at that price.

It’s not for everyone buying a car and you still need to qualify, and it’s only good until funds run out, etc. etc.

Someone asked if was a 30-year fixed with no points and his response was, “No points. No fees. 30 year fixed.”

So we know the product type and we know you won’t have to pay some excessive amount of discount points to fees to obtain the rate.

However, it’s unclear what the minimum down payment is, maximum LTV, minimum credit score, max loan amount, and so on.

It’s pretty vague and essentially just speaks to the company’s ambition to provide below-market mortgage rates.

This is exactly how the home builders navigated the past few years when mortgage rates spiked from 3% to 8%.

To cushion the blow, they leaned on forward commitments and advertised massive mortgage rate buydowns to their customers.

So even though home prices were steep and mortgage rates were no longer on sale, they could control the financing piece via the buydowns.

As a result, they could keep their asking prices elevated where they might otherwise need to be reduced.

The deals also looked spectacular when the going rate for a 30-year fixed was 7% and they were advertising 30-year fixed rates of 3.99% or even lower.

To sweeten the deal even more, they often combined temporary buydowns with permanent buydowns.

So a home buyer purchasing a new-build could get a start rate of 1.99% in year one, 2.99% in year two, 3.99% in year three, and 4.99% for the remainder of the loan term.

The 4.99% Rates Won’t Be Around Forever or Available to Everyone

I think Nejatian created a little more buzz than he bargained for with the post, which led to him answering a lot of questions from other users.

He noted that your typical mortgage has “at least 65-85 bps worth of yield” due to margin and inefficiency that goes to the many companies who “touch that mortgage.”

Opendoor can apparently “automate” much of this to bring down costs and possibly sacrifice some profit as well, at least on the mortgage side of things.

“We haven’t invented new math here. What we have done is say if our goal was to offer the lowest mortgage rate possible rather than make the most amount of money possible, what would we do?”

Again, it sounds like they’re going the home builder route and agreeing to earn less on the mortgage piece to facilitate more home sales.

Like home builders, Opendoor has inventory and that makes them a motivated seller, unlike say an existing homeowner who might only sell if it’s advantageous to do so.

Opendoor might have done the math and built in a mortgage rate discount into the home sale price where it still pencils for them.

Importantly though, Nejatian said “obviously we are not promising 4.99% rates forever or to everyone.”

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.