If you recall during the campaigning leading up to the 2024 election, Donald Trump promised to return mortgage rates to 3%, or even lower.

To anyone with an understanding of mortgage finance, or simply economics, it seemed far-fetched.

It was actually the last thing we needed, and arguably the reason why home prices surged and for-sale inventory got wiped out.

And the reason inflation surged as all those years of easy money came back to roost.

Knowing this reality meant it was time to pivot, which is perhaps why Trump proposed a 50-year mortgage on Saturday.

Trump Teases the 50-Year Mortgage. But It Isn’t Coming Soon…

While Trump’s Truth Social post garnered a ton of views, and even more conversation, that’s about all it will ever do.

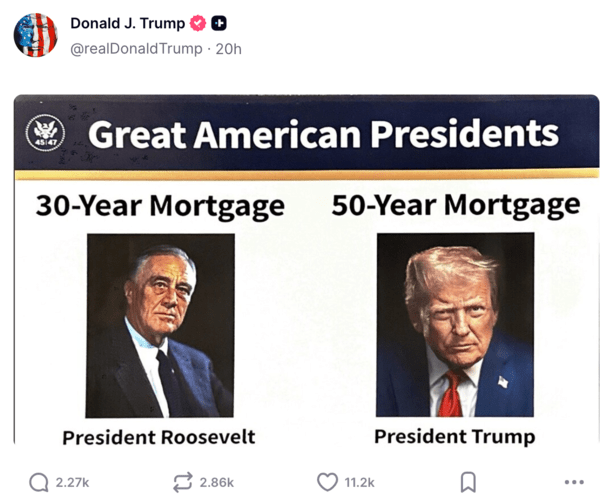

In the now infamous post, he posted a picture of “Great American Presidents” with President Roosevelt alongside himself.

Above Roosevelt’s photo was his “creation,” the 30-year mortgage, and above Trump’s the 50-year mortgage.

For the record, the Roosevelt administration established the Home Owners’ Loan Corporation (HOLC) in 1933, which ultimately led to the 30-year fixed being created.

Anyway, the message was clear; Trump is planning to bring a 50-year mortgage to the United States to solve another problem, horrendous housing affordability.

And in doing so, he’s going to make America great again. Or something.

In reality, it’s a poorly thought out post that reveals two main issues, at least for me personally.

Has Trump Heard of the ATR/QM Rule?

In the wake of the Great Financial Crisis (GFC), which was driven by shoddy mortgages and overinflated home prices, new rules were introduced to avoid another crisis.

One of the biggest ones was the Ability-to-Repay/Qualified Mortgage rule (ATR/QM), implemented in January 2014.

In short, it requires creditors to determine that a borrower can actually afford (has the documented ability to repay) the proposed housing payment put in front of them.

The QM rule goes a step further and also eliminates many risky factors, which gives lenders a presumption of compliance with the ATR requirements.

Simply put, lenders want to originate mostly QM loans because it gives them assurances and protects them from liability.

One of the key requirements for a QM rule is no loan term longer than 30 years!

So we’ve got President Trump proposing a 50-year mortgage, which is a full 20 years longer than the maximum loan term permitted under the QM rule.

That would make them non-QM loans, which inherently carry higher interest rates and are harder to come by (not all lenders offer them).

This leads me to believe that Trump has never even heard of the ATR/QM rule and that the plan is really not a plan. And just engagement bait.

In other words, don’t expect the 50-year fixed to come to a lender near you anytime soon.

For the record, even 40-year mortgages are rare post-GFC, though they do exist and I’ve seen some credit unions offer them lately.

But the reason most lenders don’t offer them is because they barely move the dial on affordability and they result in a lot more interest charged over the loan term.

The 50-Year Mortgage Idea Tells Me the Trump Admin Knows It Can’t Deliver a 3% Mortgage Rate Again

The other thing that jumped out at me is that this proposal is likely an admission, in a roundabout way, that the Trump admin knows it’s can’t deliver on its promise to bring back 3% mortgage rates.

On the road to the White House, Donald Trump told attendees at the Economic Club of New York that “we are going to get them back down to we think 3%, maybe even lower than that.”

He added that, “Young people will be able to buy a home again and be a part of the American Dream.”

A year later and the 30-year fixed is in fact lower, by about one percentage point, but nowhere close to 3%, let alone the 2s.

That has helped more existing homeowners get payment relief via a rate and term refinance.

But it hasn’t moved the dial much on monthly payments for prospective home buyers.

So it feels like they’re saying, hey, we wanted to get mortgage rates a lot lower, but it’s just not going to happen.

How about we give you a 50-year mortgage term instead? That can lower your monthly payments a little. Just ignore the fact that the total interest will more than double.

And it will take forever to pay off the loan.

I already compared 30-year and 50-year mortgages and the math wasn’t pretty.

Perhaps the worst part was that on a hypothetical $400,000 home loan, the monthly payment was only $166 cheaper!

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.