I got to thinking the other day that absent bad jobs numbers, it will be difficult for mortgage rates to move much lower anytime soon.

Arguably, they got to where they are today (~6.50% for a 30-year fixed) due to a very weak jobs print, helped on by major downward revisions.

Without that report, mortgage rates would likely still be on the higher end of 6%, closer to 7%.

Here’s the problem though; after that bombshell report, President Trump dismissed Bureau of Labor Statistics (BLS) commissioner Erika McEntarfer.

So it kind of makes you wonder if jobs data will be reliable/sugarcoated or even available for the foreseeable future, which would make it difficult to have any bearing on mortgage rates.

Can We Trust the Jobs Data Moving Forward?

President Trump recently fired McEntarfer for “faking” the jobs numbers for “political purposes,” as the July jobs report pointed to a very weak economy.

Clearly that’s not good for the President, who wants the economy to convey resilience and strength under his leadership.

The very bad jobs report instead showed that the economy is beginning to crack under the new administration, at a time when they also push global tariffs and risk even more harm.

As such, President Trump replaced McEntarfer with E.J Antoni, who appears to be more aligned with the administration, even mentioning on X to fire the Fed and pause the monthly jobs report.

Here’s the problem with that, assuming you want lower mortgage rates, which both President Trump and FHFA director Bill Pulte have stressed for a while now.

Without bad news, or at least more of the same weak economic data, mortgage rates will have a tough time moving lower.

Even if the new-look Fed becomes super accommodative again and lowers the federal funds rate multiple times, which is now expected, long-term mortgage rates may not follow.

They still need cues from actual economic data to substantiate a move lower. Without it, they won’t budge. At least not by a sizable amount.

If the jobs report is delayed, held back, or painted in a falsely-positive light, it won’t do mortgage rates any favors.

A strong jobs report would send the opposite message, that the economy isn’t doing as bad as those last reports indicated.

Or worse, is hot again, at which point any interest rate cuts would seem completely unwarranted.

It all illustrates the conflict of interest taking place at the moment, with the administration wanting a more dovish interest rate policy to reduce the country’s interest expense.

And to make housing affordability better for everyday Americans via lower mortgage rates.

While also wanting to flaunt the strength of the economy under Trump. It doesn’t work that way.

You can’t have both. You’ve got to pick one. Otherwise it risks another serious bout of inflation, something we’ve actively fought over the past few years post-ZIRP and QE.

Bringing back low mortgage rates for a short-term win risks reigniting inflation again and making our current problems that much bigger.

The Fed Rate Cuts Are Already Baked In

While the Fed doesn’t directly set mortgage rates (only its fed funds rate), Fed rate cut expectations can impact mortgage rates.

Thing is, they are telegraphed well ahead of time and never come as a big surprise. Therefore, the day of a cut or hike has no bearing on long-term mortgage rates.

Knowing the Fed is sure to cut next month means we won’t see any additional benefit to mortgage rates as a result.

This is why folks are always confused/surprised when the Fed cuts and rates go up on the day, or vice versa.

The cut/hike is already known as what happens the day of might affect rates one way or another (they don’t exist in a vacuum).

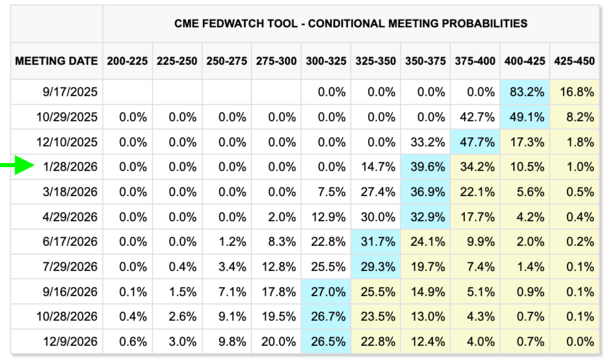

As it stands, the odds of a rate cut at the September 17th meeting are about 83%, per CME, meaning it’s highly likely.

The only way a Fed rate decision could sway mortgage rates is if something super unexpected happens, like a sure-thing cut becomes a hold. But that seems like a long shot.

And again, you need the economic data to support cuts, otherwise the bond market won’t follow suit anyway.

Without reliable economic data, we risk going down a very dangerous path that could ironically be paved with even higher mortgage rates.

Read on: Treasury Secretary Bessent Calls for Huge Rate Cuts. What Will Mortgage Rates Do?

(photo: k)

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.