I saw his seemingly straightforward question posed and was surprised I’d never really addressed it.

I’ve been writing about mortgages on this blog since 2006, so chances are I’ve covered most things.

But I rarely think in terms of a mortgage being a choice. For most, it’s compulsory, given how expensive homes are these days.

Few can buy a property with cash, so the mortgage is often a given when we’re discussing a home purchase.

That being said, we can discuss the pros and cons of getting a mortgage (and keeping it long term).

Pretty Much Everyone Needs a Mortgage

First things first. If you’re reading this and want to buy a home (or already own a home), chances are you either need a mortgage or have one.

It’s just not practical to buy a home with cash for the majority of the population.

Your average American can’t even muster a 20% down payment, so the chances of them buying a home outright is slim.

But beyond that, even those who can afford to buy a home with cash often don’t. just look at Beyoncé or Mark Zuckerberg.

When given the chance, they still opted for a mortgage. Why? Because financing is often a better play than locking up all their cash in an illiquid investment.

Their money is put to better use (theoretically) in other investments, whether it’s the stock market or something else.

All they really need to do is earn a rate of return higher than the interest rate on their mortgage.

On top of that, they get the bonus of diversification. Do you really want all or a lot of your money tied up in one thing? A home, which is susceptible to risk, such as a wildfire or a flood.

You’ve heard the phrase “don’t put your eggs in one basket,” and this applies to real estate too.

Is It Better to Be Mortgage-Free?

Okay, so we know both rich and not-so-rich often opt for a home loan instead of paying cash for a property.

But is it better to be mortgage-free, meaning eventually paying off the mortgage and holding a free and clear property?

One could argue that for the average person, yes, you should eventually pay off your mortgage.

After all, you’re paying lots of interest each month and principal, and it’s likely an expensive part of your monthly nut.

If you can remove the mortgage from your list of liabilities, you’ll have a lot more cash on hand for other expenses or investments.

And you won’t be paying a ton of interest to the bank every month anymore, which is arguably a good thing.

This is especially true if you’re at/close to retirement, as it’s generally recommended not to take a mortgage into retirement if you’ll be on a fixed income.

However, there’s a big difference between paying off the mortgage and prepaying the mortgage.

The latter means you are voluntarily and actively CHOOSING to allocate more of your money to the mortgage each month.

If this is the case, you need to consider the mortgage rate as your rate of return for making that conscious “investment.”

What About Homeowners with 2-4% Fixed-Rate Mortgages?

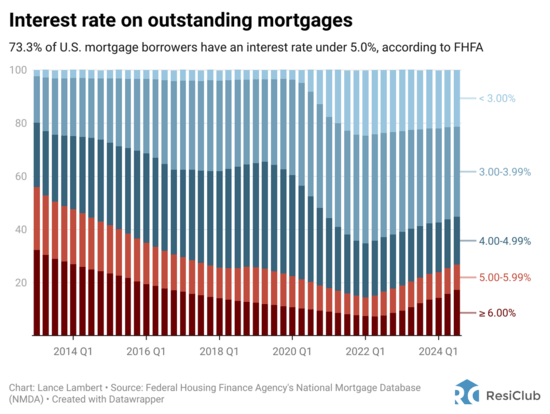

Let’s consider that pay off vs. prepay question for a moment. Today, the majority of homeowners have a mortgage rate under 5%.

At last glance, it’s something like 75% of mortgage holders have rates below 5%. And about 40% have a rate below 4%, per FHFA data compiled by Lance Lambert.

Many millions more have rates in the 1-3% range. Yes, rates that start with 1%. This is a unique phenomenon related to the Fed’s Quantitative Easing (QE) program, which has since closed.

That entailed buying trillions in mortgage-backed securities (MBS) to drive mortgage rates lower.

So in today’s day and age, homeowners likely view mortgages a lot differently than they did in the past.

The long-term average for the 30-year fixed is around 7.75%, and we all know mortgages rates in the 1980s hit 18%.

This means the argument to take out and keep a mortgage is night and day compared to those days.

If you talk to an older homeowner, they might still be biased to pay it off as quickly as possible.

But if you talk to a younger homeowner, they might say what’s the rush? I want to keep this thing as long as possible.

In other words, context matters and you need to look at your interest rate and loan type to make this determination.

There isn’t a universal mortgages are bad or mortgages are good answer. Like most things, it depends.

The home buyer today who can only get a 7% mortgage might have a completely different view of mortgages, and for good reason.

Personally, I am debt-averse, meaning I don’t like to carry any debt, but I am pro-mortgage and believe mortgage is generally a good debt.

Assess the Situation to Determine If a Mortgage Is Right for You

As noted, most of us NEED a mortgage. It’s not even a question you’ll weigh when buying a home because you won’t have any other option.

However, you will still have the option to pay off your mortgage ahead of schedule. So that is something to consider once you take out a loan.

The answer to that question will likely depend on what type of loan you have and what your interest rate is.

As a general rule of thumb, those with fixed-rate mortgages set at very low interest rates will want to keep their loans longer, possibly to maturity.

Conversely, those with higher-interest rate loans will need to sit down and consider prepaying them, assuming they can’t earn more money elsewhere, such as in a retirement account.

There is no one-size-fits-all solution, so you’ll need to put in the time and do the math to make this determination. You might even consider a financial planner to assist you with this question.

The Pros and Cons of Having a Mortgage

The Good

- Mortgages are cheap debt relative to other options

- Can get a fixed rate over a long period of time (30-year fixed)

- Allow you to put little down on a home purchase

- Creates diversification of assets with money available for other investments

- Requires homeowners insurance (generally not good to forgo it)

- Typically easy to qualify for all else equal

- Have the option to prepay or refinance if and when you want

The Bad

- There are closing costs associated with a mortgage

- It can take 30-45 days or longer to get one

- You have to pay interest each month to the lender

- Because most loans last 30 years it amounts to a ton of interest

- Could carry loan into retirement, which is generally not advised

- Requires you to carry certain level of homeowners insurance

Read on: Do I actually own my home if I have a mortgage?

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 18 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on Twitter for hot takes.