Folks have been debating so-called “mortgage rate lock-in” for years now.

It’s also known as the golden handcuffs of an ultra-low interest rate that make it difficult to move.

On the one hand, you’ve got this well-below-market mortgage rate and corresponding cheap housing payment.

On the other hand, it makes it hard to give up that rate if/when you sell, so you stay put, even if you don’t want to.

Now there’s a new program where you get a carrot; a principal reduction if you surrender that sweet rate.

Would You Give Up Your Low Mortgage Rate for a Principal Reduction?

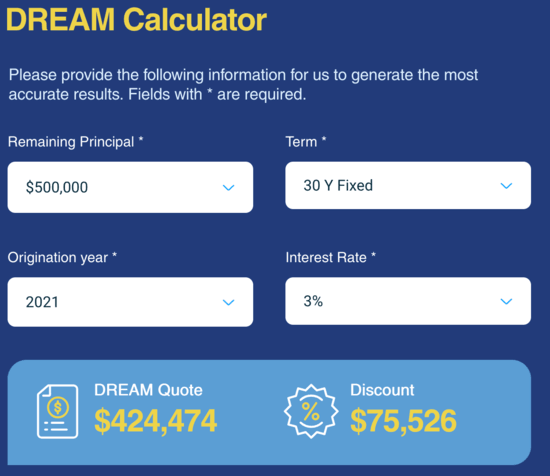

Imagine you’ve got this 2.75% 30-year fixed mortgage you took out in 2021. It’s still got a balance of $500,000 and your payment is spectacularly low.

You’ve wanted to move because your family is growing, or simply because you don’t like your home anymore. Perhaps there’s a job opportunity in a different city.

Problem is today’s mortgage rates look quite a bit different. If you sell and lose that 2.75% fixed rate, you might be looking at a 6.50% rate instead. Ouch!

This is a real dilemma countless existing homeowners face due to the ZIRP era, followed by a series of Fed rate hikes and surging bond yields, driven by inflation.

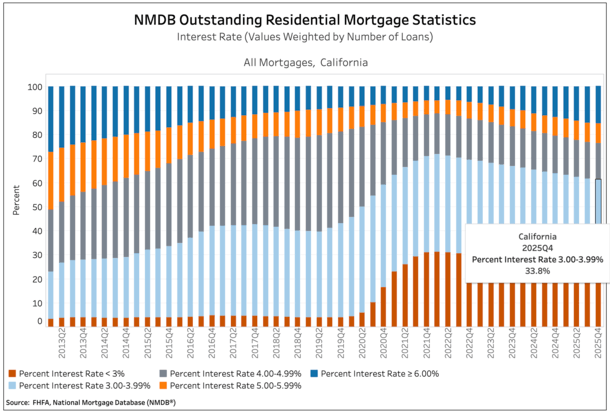

Just look at the chart above from the FHFA’s National Mortgage Database (NMDB). Roughly two-thirds of California homeowners have a mortgage rate of 3.99% or below!

Sure, they can probably sell for a pretty penny relative to what they paid, but the replacement home is likely super expensive too.

We’ve seen both home prices and mortgage rates rise in tandem, to the disbelief of many who think there’s an inverse relationship.

The New DREAM Program Can Make It More Enticing to Move

Enter the DREAM program from a fintech company called Takara.

It stands for Discount for Real Estate Affordability and Mobility, and as the name implies, provides a deal to existing home sellers who are willing to sell.

Not only is mortgage rate lock-in a problem for owners, it also means there’s less for-sale inventory for prospective home buyers.

So this gets the housing market moving again, hopefully, by eliminating the “penalty” of giving up a super low mortgage rate.

The way it works is relatively straightforward. The lender offers the borrower a discount if they sell and repay the loan early.

While you always hear that myth that the banks don’t want you to pay off your mortgage early, it couldn’t be further from the truth for the 2020-2021-era mortgages.

Those are sitting on a bank’s balance sheet somewhere, driving them crazy while prevailing markets are in some cases more than double that.

And if they remain there for another 25 years, it’s going to be very painful for the investors.

To alleviate that, you agree to sell, give up your rate, and take out a brand-new mortgage at today’s rates.

In return, you get a discount “capable of reaching 10% or more of the remaining mortgage balance.”

As seen in this screenshot, the discount could be pretty sizable, a whopping $75,000 on a $500,000 loan balance.

In other words, the bank is paying off $75,000 of your loan if you pay off your cheap mortgage ahead of time.

You then need to determine if it’s worth giving up that low rate (and the much lower interest expense) for the ability to move.

This Is Why I Say to Think Before Voluntarily Prepaying a Cheap Mortgage

There are all these posts online about how someone paid off a mortgage ahead of schedule.

And how much they saved. But what’s the opportunity cost? Could that “investment” in the mortgage gone further someplace else?

When you voluntarily agree to pay off a 2-3% mortgage early, you are essentially locking in an investment return of just 2-3%.

It doesn’t sound so good does it? Especially when stocks are rising double-digits, and even a plain old savings account earns 3-4% these days.

The fact banks are willing to pay you to pay off a cheap mortgage ahead of time tells you everything you need to know.

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.